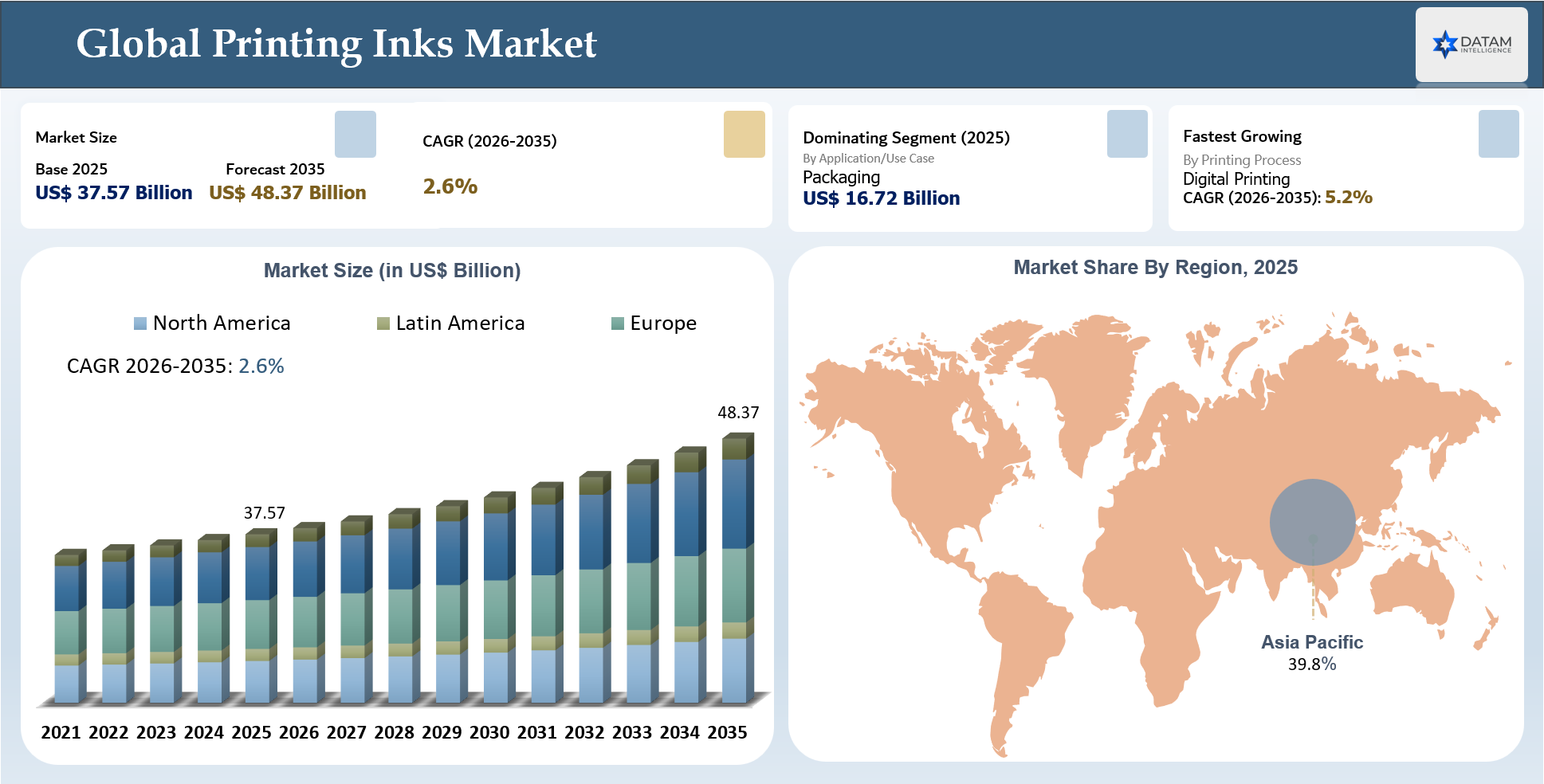

Printing Inks Market Size

The Global Printing Inks Market stood at US$ 37.57 billion in 2025 and is expected to reach US$ 48.37 billion by 2035, growing with a CAGR of 2.6% during the forecast period 2026-2035.

The global printing inks market is entering a structural transition driven by regulatory and sustainability-led reformulation, rather than simple volume growth. Food-contact safety, VOC reduction, recyclability, low migration, odor control and chemical compliance are becoming key purchasing criteria for packaging converters, brand owners and commercial printers. This shift is especially visible in food and beverage, pharmaceutical, personal care, flexible packaging, labels and e-commerce packaging applications, where ink performance directly affects packaging safety, shelf appeal, compliance and production efficiency.

This transition is changing competitive advantage across the value chain. Ink manufacturers are investing in water-based, low-VOC, bio-based, UV-curable, LED UV-curable, electron beam-curable and low-migration inks to meet evolving packaging and labeling requirements. As buyers move away from commodity ink selection, suppliers with strong reformulation capabilities, technical service, substrate-specific customization, color management expertise and regional supply reliability are better positioned to capture premium growth.

Key Takeaways

- The Global Printing Inks Market was valued at US$37.57 billion in 2025 and is projected to reach US$48.37 billion by 2035.

- The market is expected to grow at a CAGR of 2.6% during 2026-2035, supported by packaging demand, sustainable ink adoption, and digital printing growth.

- Asia-Pacific held the highest market share at 39.8% in 2025, supported by large packaging conversion capacity, strong consumer goods production, and expanding e-commerce packaging demand.

- Asia-Pacific is expected to remain the fastest-growing region, driven by growth in flexible packaging, labels, food packaging, pharma packaging, and rising adoption of low-VOC and water-based inks.

- Packaging was the largest application/use case segment in 2025, valued at approximately US$16.72 billion, supported by demand from food, beverage, pharma, personal care, and e-commerce packaging.

- Digital Printing is projected to be the fastest-growing printing process, expanding at an estimated 5.2% CAGR during 2026-2035, driven by short-run packaging, personalization, QR-enabled labels, and variable-data printing.

- Sustainability is becoming a key purchasing factor, with buyers shifting toward water-based, low-VOC, bio-based, UV-curable, LED UV-curable, and low-migration ink systems.

- Procurement decisions are increasingly based on color consistency, substrate compatibility, drying or curing speed, food-contact safety, VOC profile, technical support, and supply reliability.

- The market has a strong competitive concentration, with major players including DIC Corporation, Flint Group, Siegwerk Druckfarben AG & Co. KGaA, artience Co., Ltd., SAKATA INX CORPORATION, and hubergroup.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 37.57 Billion | |

| 2035 Projected Market Size | US$ 48.37 Billion | |

| CAGR (2026-2035) | 2.6% | |

| Largest Market | Asia-Pacific | |

| Fastest Growing Market | Asia-Pacific | |

| By Ink Type | Solvent-Based Inks, Water-Based Inks, Oil-Based Inks, Latex Inks, and Others | |

| By Curing Type | Conventional Drying Inks, UV-Curable Inks, LED UV-Curable Inks, Electron Beam-Curable Inks, Oxidative Drying Inks, and Others | |

| By VOC Level | Zero VOC Inks, Low VOC Inks, and High VOC Inks | |

| By Bio-Based Content | Bio-Based Inks and Non-Bio-Based Inks | |

| By Printing Process | Flexographic Printing, Gravure Printing, Offset Lithography, Digital Printing, Screen Printing, Letterpress Printing, and Others | |

| By Resin Type | Acrylic, Polyurethane, Polyamide, Nitrocellulose, Modified Rosin, Hydrocarbon Resin, Epoxy, Polyester, and Others | |

| By Application/Use Case | Packaging, Labels and Tags, Commercial Printing, Publications, Decorative Printing, Textile Printing, Security Printing, Industrial Printing, and Others | |

| By Substrate | Paper and Paperboard, Plastics and Films, Metal, Glass and Ceramics, Textile, Wood, and Others | |

| By End-Use Industry | Food and Beverages, Pharmaceuticals, Personal Care and Cosmetics, Consumer Goods, Publishing and Commercial Printing, Textiles and Apparel, Electronics, Automotive, Industrial Goods, and Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

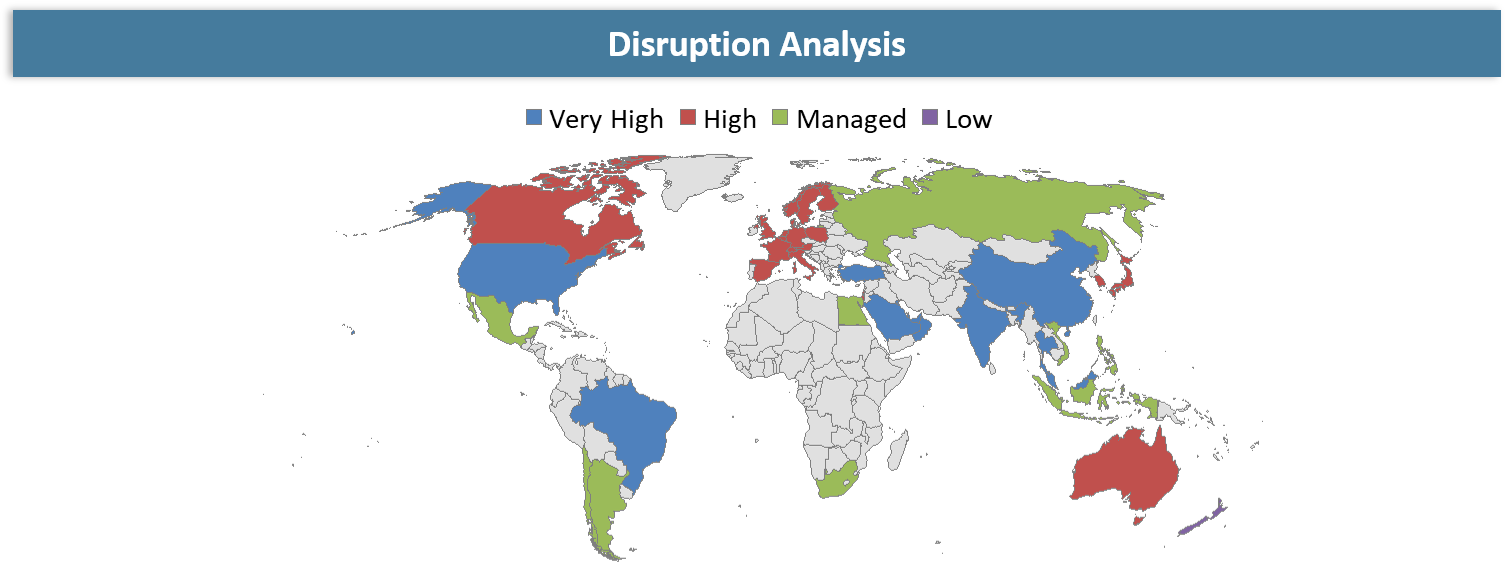

Disruption Analysis

Sustainability, Digital Printing and Regulatory Compliance Are Reshaping Ink Innovation

Disruption in the Global Printing Inks market is arising due to the transition from conventional solvent-based inks to sustainable, compliant and application-oriented products. As brand owners, packaging converters and printers face increased pressure to lower VOC emission levels, support recyclable packaging, ensure food contact compliance and adopt low-migration technology, this trend is boosting growth in water-based inks, bio-based inks, UV-cured inks, LED-cured inks and digital ink markets. Solvent-based and commodity offset inks markets are facing challenges on account of increasing adoption of newer technologies and formulations.

Disruptions arising out of digital printing, smart packaging solutions and advanced printing quality controls are also shaping up ink formulations across applications. Factors such as short-run packaging, variable printing, QR-coded labels, anti-counterfeiting measures and personalized packaging trends are leading the way towards new ink formulations and usage patterns. While rising raw materials price volatility, pigment shortages, high resin costs and increasingly stringent chemicals regulations are putting pressure on suppliers to innovate rapidly and develop localized supply chain strategies, firms with advanced R&D capabilities and technical services will have an advantage over their peers.

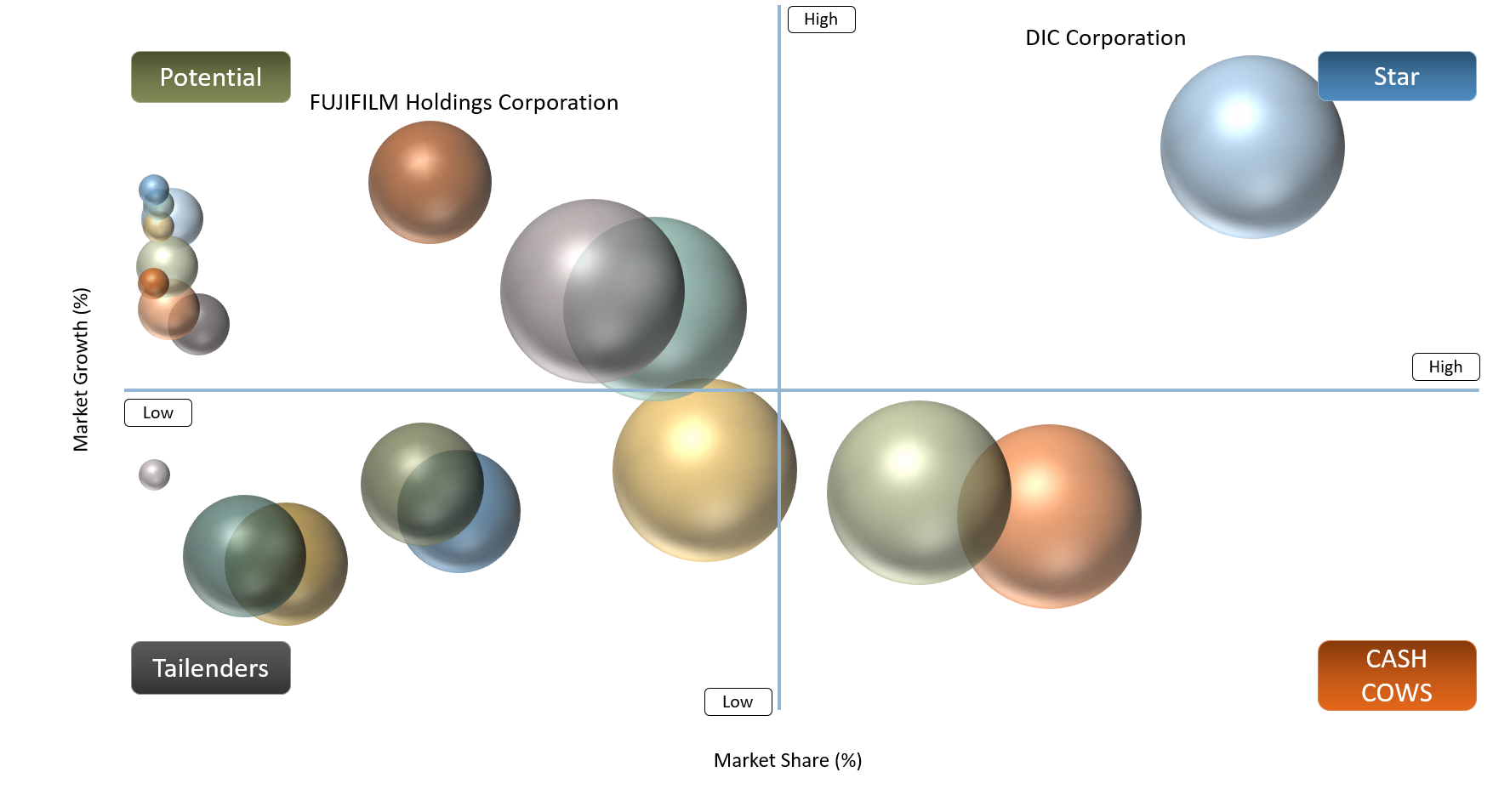

BCG Matrix: Company Evaluation

As for the BCG matrix, In the Global Printing Inks Market, Stars are those that have a large-scale footprint on the global stage, an extensive portfolio of inks, brand influence, superior formulation skills, and dominance in packaging, commercial, label, digital, and specialty ink market segments. Among other candidates, DIC Corporation, Flint Group, Siegwerk Druckfarben AG & Co. KGaA, artience Co., Ltd., SAKATA INX CORPORATION, and hubergroup fit into the Stars category, due to their global client base, extensive packaging ink portfolio, focus on sustainability, regional manufacturing facilities, and capability to serve converters, brand owners, and commercial printers using various printing technologies.

Cash Cows are those that have well-established product offerings, solid client relations, and significant importance in certain printing ink types including UV inks, specialty coatings, security inks, offset inks, and industrial printing inks. Candidates for this category include T&K TOKA CO., LTD., ALTANA AG, Zeller+Gmelin, Epple Druckfarben AG, SICPA HOLDING SA, and Dainichiseika Color & Chemicals Mfg. Co., Ltd. These firms enjoy solid defensible positions in certain niches within the Global Printing Inks Industry that are commercially important despite maturity.

Question Marks are organizations which possess increasing significance in digital printing inks, proprietary ink systems, and wide format printing, though with comparatively narrow positioning in terms of the entire traditional printing ink industry. FUJIFILM Holdings Corporation, Epson, Mimaki, and HP may be considered as Question Marks due to the fact that their ink position is significantly dependent on the advancement of digital printing. This future positioning would depend on the rate at which digital printing grows in packaging, labeling, textile, and industrial printing.

Market Dynamics

Packaging Converters Are Shifting Toward High-Performance Inks for Faster Line Speeds and Lower Rejection Rates

Packaging converters are increasingly evaluating their printing ink choices on the basis of efficiency rather than color capabilities. With the increase in speed of packaging lines and the degree to which they rely on automation, efficient inks have to be those that offer stability in terms of viscosity, high levels of adhesion, good color density, quick curing/drying time, as well as efficient application on paperboard, film, flexible packaging, labels, and corrugated materials. Poor ink performance could result in smudging, blocking, color shifting, rubbing, material incompatibility, and mechanical failure. All these factors directly translate into inefficiencies and higher costs.

This trend is driving greater interest in the use of waterborne, UV-cured, LED UV-cured, low migration, and even material-specific ink formulations that can accommodate high-speed flexographic, rotogravure, offset, and digital printing processes. Inks from vendors who offer technical assistance, color management, quick troubleshooting, and formulation options are preferred to vendors providing commodity ink products. As converters face tighter delivery timelines, sustainability targets, and brand quality expectations, ink performance is becoming a direct driver of productivity, compliance, and customer retention.

Stricter VOC, Migration and Chemical Safety Regulations Are Increasing Reformulation Costs for Ink Manufacturers

Regulatory pressures are becoming another important restraint in the Global Printing Inks market, particularly for packaging inks used in applications involving food, beverages, pharmaceuticals, cosmetics/personal care, and consumer goods. The growing pressure on ink companies to meet regulatory requirements in areas such as VOC content, chemical toxicity, heavy metals, solvents, smell, migration, and contact with food is expected to be restraining. Consequently, traditionally solvent-intensive and highly migratory inks are coming under greater scrutiny, and their reformulation has to be done while maintaining good adhesive properties, opacity, fast drying, rub resistance and printability.

This will add to the expenses involved in R&D, substituting materials, testing, certification, and customer approval. New formulations that include the use of water, low VOCs, low migration, renewable resources, and energy-cured resins need different binders, pigments, additives, and photoinitiators. In addition, smaller firms may find it difficult to bear these expenses, whereas larger firms have to contend with long qualifying periods with their converters and customers. This particular restraint does not impact only regulation but also price competitiveness, product launches, and margins in competitive markets.

Segmentation Analysis

The global printing inks market is segmented based on the ink type, curing type, VOC level, bio-based content, printing process, resin type, application/use case, substrate, end-use industry, and region.

Packaging Segment Dominates the Global Printing Inks Market Due to Strong Demand from Food, Beverage, Pharma and E-Commerce Packaging

The packaging application segment leads the Global Printing Inks Market due to its consistent demand that comes from various types of flexible packaging, labels, folding cartons, corrugated boxes, pouches, sleeves, and pharmaceutical packaging. Brands from the F&B, health & hygiene, healthcare, and FMCG sectors need printing inks to enhance their presence, increase identification, comply with regulatory requirements, trace their products, and differentiate themselves. With packaging becoming more brand-oriented, compliance-driven, and sustainable, the quality of ink used influences the quality of packaging, safety of the products, efficiency in production, and consumer satisfaction.

There has also been an evolution within this segment from simple ink usage to performance-driven and compliant inks. Packaging producers are beginning to adopt water-based, low-VOC, UV-curable, LED-UV curable, low-migration, and digital inks to boost productivity, guarantee food safety, ensure packaging can be recycled, maintain uniform colors, and minimize rejection rates. E-commerce is bringing new demand dynamics by way of corrugated printing, shipping labels, variable data printing, and packaging graphics, making packaging the most appealing area for ink manufacturers.

Geographical Penetration

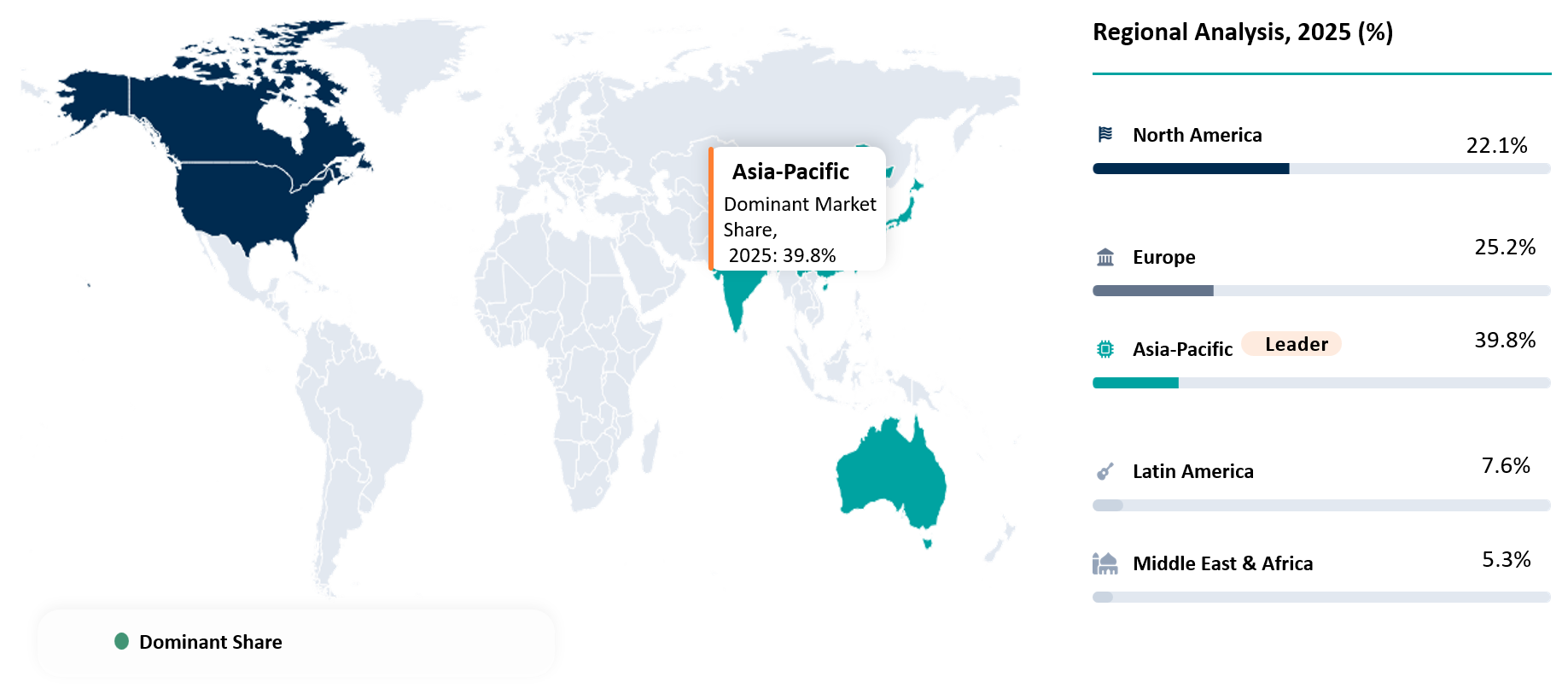

Asia-Pacific’s Packaging Scale and Sustainable Ink Transition Are Driving Regional Leadership

Asia-Pacific is the leading and the fastest-growing region in the Global Printing Inks Market, representing approximately 39.8% market share in the region. This leadership of the region is fueled by the large packaging conversion base in the region, robust consumer goods manufacturing infrastructure, and high demand for printing in flexible packaging, labeling, corrugated containers, and commercial print. The key demand centers in the region include China, India, Japan, South Korea, Indonesia, Vietnam, and Thailand. Demand drivers include packaged foods, beverages, pharmaceutical products, personal care, textile packaging, and e-commerce logistics.

There is a shift in the regional growth dynamics from volume growth to performance-driven ink usage. Packaging converters are shifting towards more efficient ink formulations, including water-based, low-VOC, UV-curable, LED-UV curable, digital, and low-migration ink. India and Southeast Asia offer particularly good opportunities due to growing local packaging manufacturing capabilities alongside higher regional procurement of goods by global brand owners. Nevertheless, raw material price volatility is a key margin challenge due to reliance on petrochemical-based components including solvents, resins, additives, coatings, and adhesives used in the manufacture of printing inks.

U.S Printing Inks Market Trends

The U.S. Printing Inks Market is shifting toward a more specialized, packaging-led demand structure, where growth is increasingly tied to food and beverage packaging, pharmaceutical labeling, personal care packaging, corrugated boxes, folding cartons, and e-commerce shipping formats. Traditional publication and commercial print categories remain under pressure, but packaging, logistics, and variable-data printing are creating more resilient demand for high-performance ink systems. U.S. retail e-commerce sales reached USD 302.3 billion in Q1 2026 and represented 16.8% of total retail sales, strengthening the need for printed shipping labels, corrugated packaging, flexible packaging, and traceability-focused print applications.

The market is also moving from commodity ink procurement toward performance, compliance, and sustainability-led purchasing. Converters are prioritizing water-based inks, UV and LED-curable inks, low-migration formulations, low-VOC inks, and digital printing inks that support faster curing, food-contact safety, color consistency, recyclability, and shorter production runs. Supplier differentiation will increasingly depend on technical service, substrate-specific formulation capability, color management, local supply reliability, and the ability to support brand owners with sustainable and regulation-ready packaging solutions.

Japan Printing Inks Market Outlook

Japan’s Printing Inks Market is evolving as a mature but high-value market, where demand is increasingly linked to packaging quality, functional labeling, sustainability, and precision printing rather than broad volume expansion. Growth is supported by food packaging, pharmaceutical labels, cosmetics packaging, convenience-store retail formats, flexible packaging, and digital label printing. Japan’s export base also highlights its relevance in the regional ink value chain, with Japan exporting USD 188.36 million of black printing ink in 2024, equivalent to around 12.07 million kg, led by shipments to the U.S., China, the Netherlands, the Philippines, and Vietnam.

The market outlook is shifting toward water-based, low-VOC, UV-curable, LED UV-curable, low-migration, and digital inks as converters respond to food-contact safety, recyclability, and brand-quality requirements. However, Japan’s ink value chain remains exposed to petroleum-derived raw material risks. In 2026, Calbee announced temporary black-and-white packaging for 14 products due to ink-related supply pressure linked to naphtha sourcing, with Reuters reporting that Japan imports about 40% of its naphtha from the Middle East. This reinforces the need for raw material resilience, formulation flexibility, and secure sourcing strategies in Japan’s premium printing inks market.

Competitive Landscape

The Global Printing Inks Market has moderate consolidation with competition among large ink manufacturing companies from across the world, along with specialized formulation providers. DIC Corporation, Flint Group, Siegwerk Druckfarben, artience Co., Ltd., SAKATA INX CORPORATION, and hubergroup have significant competitive positioning due to their extensive product portfolio consisting of packaging inks, commercial printing inks, labels, coatings, and sustainable ink solutions. The companies compete in formulating high-performing products based on their consistency, substrate compatibility, regulatory compliance, supply chain networks regionally, and customer support services.

Market includes specialized and innovative competitors like T&K TOKA CO., LTD., ALTANA AG, FUJIFILM Holdings Corporation, Zeller+Gmelin, Wikoff, Epple Druckfarben AG, SICPA HOLDING SA, Dainichiseika Color & Chemicals, Nazdar, Epson, Mimaki, and HP. Such players are strengthening the level of competition by specializing in UV curable inks, digital printing inks, security inks, industrial ink applications, screen printing inks, and wide format ink technologies. Competitive advantage among these players depends on sustainability, low VOC ink, digital printing inks, and safe packaging solutions.

Recent Developments

- April 2026: Sun Chemical, a member of the DIC Group, launched the AquaHeat platform, a new generation of food-safe, bio-based printing inks for high-temperature food applications, supporting commercial baking and food-service packaging opportunities.

- March 2026: Siegwerk Druckfarben AG & Co. KGaA signed a definitive agreement to acquire Hi-Tech Inks, an Indian producer of flexographic and gravure printing inks, strengthening its position in India’s flexible packaging market and creating a combined business with more than 20% market share.

- November 2025: artience Group, through Toyo Ink India, announced plans to expand liquid ink production at its Gujarat plant, with the new facility scheduled for 2028 and expected to increase total production capacity by approximately 1.5 times to meet India’s packaging demand.

- October 2025: Flint Group showcased its AQUACode inks and coatings at CorrExpo 2025, highlighting water-based ink and coating technologies for paper and board printing that support recyclability, reduced waste, higher press speeds and consistent print quality.

- September 2024: Mimaki unveiled new printer technologies, including the CJV200 Series using its new SS22 eco-solvent ink, which excludes increasingly regulated GBL ingredients and supports outdoor durability with a more environmentally friendly paper cartridge format.

- May 2024: Sun Chemical, a member of the DIC Group, showcased sustainability expertise at drupa 2024, including EB-curable ink technologies designed to reduce solvent usage and improve the recyclability profile of packaging materials.

- March 2024: HP Inc. launched new HP Indigo digital presses, including the HP Indigo 120K, 18K and 7K Secure Digital Press, strengthening digital commercial, packaging and security printing capabilities supported by HP Indigo ElectroInk technology.

Printing Inks Market Value Chain Analysis

The printing inks market value chain begins with suppliers of pigments, resins, solvents, additives, photoinitiators, and specialty chemicals that form the foundation of ink formulations. These raw materials are processed by ink manufacturers that develop customized products for packaging, labels, commercial printing, textile printing, security printing, and industrial applications.

Downstream participants include packaging converters, commercial printers, label manufacturers, and brand owners that use printing inks to improve product identification, regulatory compliance, visual appeal, and consumer engagement. The increasing adoption of recyclable packaging, low-migration technologies, and sustainable printing practices is creating stronger collaboration across the value chain.

Key Stakeholders Across the Value Chain

- Pigment and Colorant Suppliers

- Resin and Polymer Manufacturers

- Solvent and Additive Producers

- Printing Ink Manufacturers

- Packaging Converters

- Commercial Printers

- Label and Flexible Packaging Producers

- Brand Owners

- Retailers and End Users

Value Creation Areas

- Sustainable ink formulation

- Food-contact compliance

- Low-VOC technologies

- Color management solutions

- Digital printing compatibility

- Supply chain localization

- Technical support services

AI Impact Analysis

AI is slowly taking shape in the Global Printing Inks Market by aiding formulation development, color matching, process control, and defect elimination. Manufacturers in the industry are employing AI-based systems to study the pigments' behavior and properties along with other qualities such as compatibility of resins, viscosity, drying ability, and substrate interaction. This helps them save time spent on experimenting and come up with custom-made formulations quicker. Color management based on AI enables printers to produce consistent prints across substrates, locations, and printing technologies.

The impact is also visible in procurement, quality control, and sustainability planning. AI-driven demand forecasting can help ink suppliers manage raw material volatility, optimize inventory, and reduce production waste. In printing operations, machine vision and predictive analytics can detect print defects, curing issues, color deviations, and ink transfer problems in real time. Over time, AI will support the shift toward low-VOC, low-migration, water-based, UV-curable, and bio-based ink systems by accelerating testing, compliance validation, and performance optimization.

White Space Opportunities

For the Global Printing Inks Market, there is good white space in ink systems driven by sustainability and compliance, which include water-borne, low-VOC, low migration, bio-based, and both UV-cured and LED-cured inks. The need to provide an ink solution for recyclable packaging, safe for contact with food products, fast curing, reduced odors, attractive shelf appearance, and minimized environmental impact is driving interest from packaging converters and brand owners. There is therefore significant opportunity for companies that produce high-quality inks for flexible packaging, labels, folding carton, corrugated, and e-commerce packaging.

Specialized inks for digital printing, smart packaging, security printing, and industrial use are also creating lucrative growth segments. The growing requirements for customized packaging, short-run packaging, anti-counterfeiting labels, QR-coded packaging, and variable data printing are driving the need for specialized inks for digital printers, specialized substrates, functional coatings, and fast high-speed automated printers. Potential opportunities are also arising in emerging economies of the Asia Pacific region, Latin America, Middle East, and Africa regions as the packaged foods, pharmaceuticals, personal care products, and retail industries embrace new technologies. Companies that combine formulation innovation, technical support, local production, regulatory expertise, and substrate-specific customization can move beyond conventional commodity ink sales.

DMI Opinion

As per the findings of DataM, the Global Printing Inks Market is shifting away from a volume-driven commoditized product into a performance-driven specialty materials market. The greatest opportunities for future growth are in sectors where print performance affects brand competitiveness, including packaging, labels, flexible packaging, food and beverages, pharmaceuticals, personal care, and e-commerce markets. Adhesion, drying, color match, migration risk, VOC content, compatibility and customer support have replaced price alone in buyers' decision-making criteria.

DMI forecasts sustainability and digitization to be the drivers of competitive success through 2030. Waterborne, low VOC, bio-based, UV curable, LED UV curable, low migration and digital inks will become more popular as packaging producers and brand owners embrace recycling initiatives and regulatory demands as well as short run customizations. Formulation capability, supply security in key regions, color matching capabilities and technical support specific to the application will distinguish successful companies from their competitors.

Why This Report Matter in 2026?

The Global Printing Inks Market is set to become more strategic for 2026, with packaging, labeling, commercial, and industrial printing customers focusing not only on color but on safety, speed, and environmental sustainability of the inks they use. They will be challenged to optimize their shelf appeal, minimize VOC emissions, develop recyclable packaging, fulfill food contact and migration requirements, and achieve high-speed consistent printing, making their choice of ink directly linked to packaging quality, compliance, efficiency, and brand identity.

The importance of this report lies in the significant change currently happening within the market, shifting from traditionally solvent-based formulations to water-based, UV, digital, low migration, and bio-based inks. Buyers require insights into opportunities by technology type, substrate, application, and geography. The report will help ink manufacturers, packaging converters, raw materials companies, and investors understand growth areas, benchmark themselves against their peers, prioritize procurement decisions, and create expansion strategies.

Why Choose DataM?

- Printing Inks Value Chain Analysis: Comprehensive assessment of the entire value chain of printing inks, including raw materials, pigments, resins, solvents, additives, ink formulation, print technology, substrate, converter, brand owner, packager, printer, and end-user.

- Product & Technology Evaluation: Review of important ink technologies, including solvent inks, aqueous inks, UV curable inks, electron beam inks, oil inks, digital inks, low-migration inks, bio-based inks, and specialty ink sets, to determine commercially viable opportunities for growth.

- Application/Use Cases & End User Evaluation: Follows the demand for ink products in packaging, labels & tags, commercial printing, publication, textile printing, decorative printing, security printing, industrial printing, food & beverages packaging, pharmaceuticals, cosmetics, consumer goods, and e-commerce packaging.

- Regulatory, Sustainability & Compliance Evaluation: Reviews the effect of food contact safety standards, low-VOC compliance, migration, recyclability, solvent reduction, hazardous material restriction, packaging regulation, and sustainable branding on regional ink product acceptance.

- Competitive Strategy Benchmarking: Monitors leading players such as DIC Corporation, Flint Group, Siegwerk Druckfarben AG & Co. KGaA, artience Co., Ltd., SAKATA INX CORPORATION, and hubergroup based on product portfolio strength, ink technology innovation, sustainability positioning, regional manufacturing presence, customer partnerships, and ability to serve packaging, labels, commercial printing, and specialty printing applications.

- Pricing, Procurement, and Market Access Assessment: Highlights the importance of consumer needs, fluctuations in raw materials costs, market trends in inks, key considerations for supplier selection, procurement methods used by packaging converters, technical support services offered, substrate performance, availability, and potential contracts.

- Growth Opportunities and New Product Development: Highlights the untapped opportunities in sustainable packaging inks, water-based inks, UV & LED inks, digital printing inks, low migration inks for food packaging applications, inks for flexible packaging applications, label inks, security inks, and other regions.

Key Procurement Priorities and Buyer Evaluation Criteria

- Buyers in the Global Printing Inks Market are increasingly prioritizing ink systems that deliver strong print quality, color consistency, substrate adhesion, faster drying or curing performance, rub resistance, low odor, low migration, and reliable performance across high-speed printing lines.

- Procurement decisions are shifting toward integrated ink and coating solutions that support flexographic, gravure, offset, digital, screen, and packaging printing workflows, while also meeting brand requirements for visual appeal, shelf impact, regulatory compliance, and sustainability.

- Packaging converters, commercial printers, label manufacturers, publishing companies, textile printers, and industrial printing users are evaluating vendors based on ink performance, batch-to-batch consistency, technical support, compatibility with substrates and printing equipment, food-contact safety, VOC profile, curing efficiency, pricing stability, and supply reliability.

- Vendors with strong capabilities in water-based inks, UV-curable inks, low-migration packaging inks, digital printing inks, sustainable formulations, color management, and customized ink development are better positioned to win long-term contracts as buyers move toward quality-driven, compliant, and cost-efficient printing solutions.