Ultrasonic Aspirator Market Size and Trends

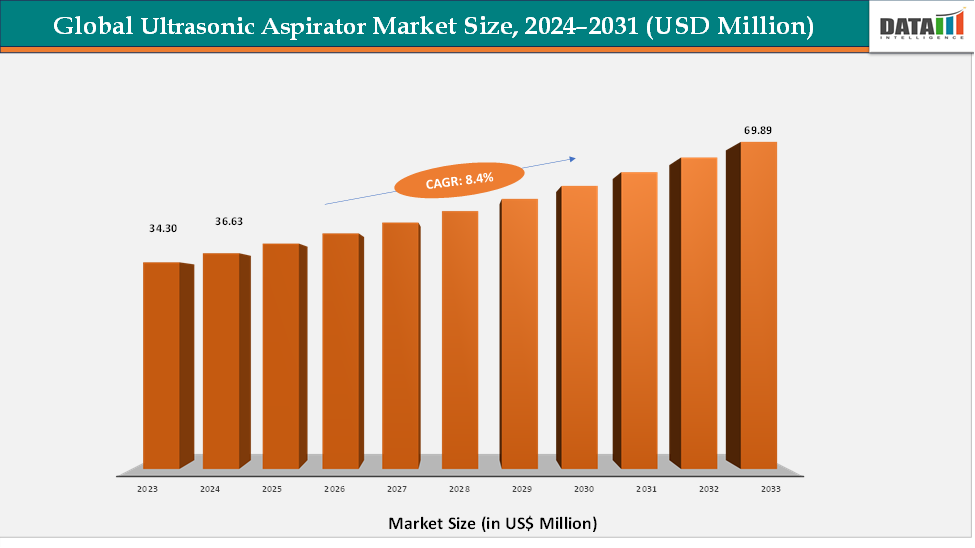

The global ultrasonic aspirator market reached US$ 234.6 million in 2023, with a rise to US$ 247.27 million in 2024, and is expected to reach US$ 414.56 million by 2033, growing at a CAGR of 6.7% during the forecast period 2025–2033. The market is driven by the increasing volume of neurosurgical and oncological procedures, technological advancements in precision surgery, and the growing adoption of minimally invasive techniques. Innovations such as multifunctional aspirators with integrated cutting, coagulation, and irrigation functions, along with robotics-compatible platforms, are expanding their clinical utility beyond neurosurgery into oncology, orthopedics, and reconstructive surgeries. For instance, Stryker offers its next-generation Sonopet iQ system, designed to deliver enhanced precision and ergonomic efficiency for complex cranial and spinal procedures. Thus, the rising surgical demand, continuous device innovation, and expanding application areas are driving the ultrasonic aspirator market.

Key Market highlights

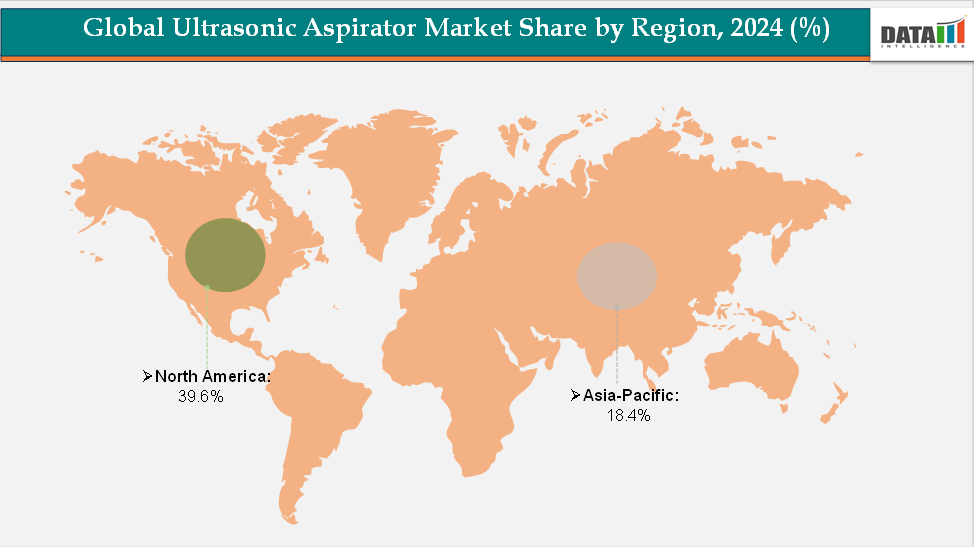

North America holds 39.6% of the ultrasonic aspirator market, driven by advanced healthcare infrastructure, high neurosurgical and oncology case volumes, and strong presence of key manufacturers.

Asia-Pacific accounts for 18.4% and is the fastest-growing region, supported by rising cancer and neurological surgeries, expanding healthcare access, and strong growth in China, India, and Japan.

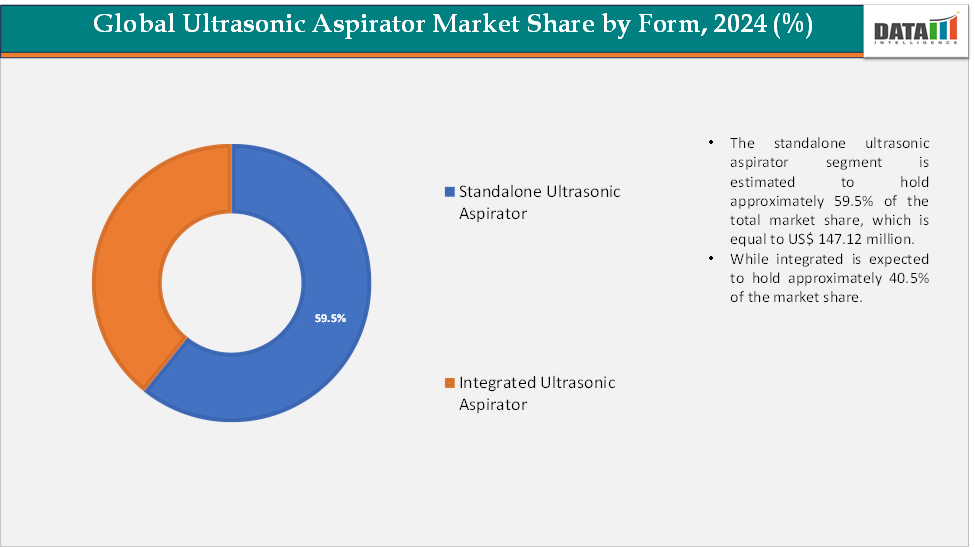

Standalone ultrasonic aspirators dominate with 56.7% share, favored for their portability, cost-effectiveness, and wide applicability across surgical specialties.

Market Size & Forecast

2024 Market Size: US$ 247.27 Million

2033 Projected Market Size: US$ 414.56 Million

CAGR (2025–2033): 6.7%

North America: Largest market in 2024

Asia Pacific: Fastest-growing market

Market Dynamics

Driver: Rising Neurosurgical and Oncological Procedures

The increasing number of neurosurgical and oncological procedures worldwide is one of the most important factors fueling demand for ultrasonic aspirators. For instance, according to the American Association of Neurological Surgeons, over 13.8 million neurosurgical procedures are performed each year. In neurosurgery, the rising prevalence of brain tumors, traumatic brain injuries, and complex spinal disorders has created a strong need for highly precise and tissue-selective surgical tools. For instance, according to the National Institute of Health, in 2022, 322,000 new cases of brain and CNS tumors were estimated globally. By world region, the highest incidence rate was seen in North America, Eastern Asia, and Western Europe. Africa had relatively lower incidence rates. Ultrasonic aspirators provide surgeons with the ability to fragment and aspirate pathological tissue while sparing critical surrounding structures, which is essential in delicate brain and spinal surgeries where even minimal collateral damage can lead to severe functional impairment. This precision advantage is a major reason for their growing adoption in tertiary hospitals and specialized neurosurgical centers.

Oncology further reinforces this trend, as the global cancer burden continues to rise, particularly liver, pancreatic, and kidney tumors that often require surgical debulking or resection. Ultrasonic aspirators enable safe and efficient tumor removal with reduced intraoperative blood loss, shorter procedure times, and improved patient outcomes. With cancer surgeries becoming more common due to advances in early detection and wider access to surgical oncology services, the demand for such devices is expected to grow steadily. Additionally, the shift toward minimally invasive and organ-preserving surgical techniques makes ultrasonic aspirators even more valuable, as they combine cutting, aspiration, and coagulation in a single device, improving efficiency and reducing surgical trauma. Together, these factors establish rising neurosurgical and oncological procedures as a powerful driver of market expansion.

Restraint: Availability of Alternative Surgical Tools

The widespread availability of alternative surgical tools poses a significant challenge to the growth of the ultrasonic aspirator market. While ultrasonic aspirators offer precision and selectivity in tissue removal, many hospitals and surgical centers rely on more established and cost-effective devices such as electrosurgical units, surgical drills, laser systems, and radiofrequency-based instruments. These alternatives are often less expensive, require minimal training, and are already widely available in most operating rooms, making them a preferred choice for healthcare providers working in cost-sensitive settings.

For more details on this report, Request for Sample

Segmentation Analysis

The global ultrasonic aspirator market is segmented by type, application, end-user, and region.

Type:The standalone ultrasonic aspirator segment is estimated to have 59.5% of the ultrasonic aspirator market share.

The standalone ultrasonic aspirator segment currently holds a dominant share of the market. These systems are widely adopted because of their versatility, portability, and cost-effectiveness compared to integrated systems. Standalone aspirators are easy to install, require less infrastructure, and can be deployed across a wide range of surgical settings, from large hospitals to smaller clinics and ambulatory surgical centers. Their modular design, compatibility with different surgical specialties, and relatively lower capital investment make them the preferred choice in both developed and developing markets.

Moreover, the recurring demand for consumables such as probes and handpieces further strengthens the revenue stream for manufacturers in this segment. The ability to deliver advanced tissue-selective removal without the need for large-scale integration has ensured that standalone aspirators remain the backbone of the market..

The integrated ultrasonic aspirator segment is estimated to have 40.5% of the ultrasonic aspirator market share.

The integrated ultrasonic aspirator segment, while smaller in current market share, is gaining momentum, particularly in technologically advanced healthcare systems. These devices are often embedded within multifunctional surgical workstations or robotic platforms, offering enhanced efficiency and streamlined workflow for complex procedures. Their adoption is higher in tertiary care hospitals and academic medical centers, where there is a strong emphasis on advanced surgical technologies and comprehensive patient care.

Although the high cost and infrastructure requirements limit their use in resource-constrained settings, integrated aspirators are expected to experience faster growth over the coming years. This growth will be driven by the rising adoption of robotic-assisted surgery, demand for multifunctional devices, and the push toward advanced operating room ecosystems in North America, Europe, and Japan.

Geographical Analysis

The North America ultrasonic aspirator market was valued at 40.1% market share in 2024

North America is expected to maintain its dominant position in the ultrasonic aspirator market, supported by advanced healthcare infrastructure, strong adoption of cutting-edge surgical technologies, and a high volume of complex neurosurgical and oncology procedures. The region benefits from early adoption of minimally invasive surgical techniques, a strong presence of leading manufacturers, and favorable reimbursement policies that encourage hospitals to invest in high-value surgical devices.

Within North America, the United States leads the market due to its large patient pool, high prevalence of neurological disorders and cancer, and significant expenditure on healthcare innovation. According to the report by the National Institute of Health in 2025, 2025 2,041,910 new cancers are projected to occur in the United States. The U.S. also has a well-established ecosystem of academic medical centers, specialized surgical hospitals, and research institutions, which accelerates both device adoption and continuous product improvement. Additionally, robust FDA regulatory approvals and consistent product launches by companies such as Stryker and Integra LifeSciences further reinforce the country’s dominance in this market.

The Europe ultrasonic aspirator market was valued at 26.8% market share in 2024

Europe represents a significant market for ultrasonic aspirators, supported by advanced healthcare infrastructure, strong adoption of innovative surgical tools, and a high volume of neurosurgical and oncology procedures across the region. Countries such as the UK, France, and Italy contribute meaningfully to market growth, but Germany stands out as the dominant market, owing to its well-established network of specialized hospitals, high investment in medical technology, and strong focus on neurosurgery and oncology care. German hospitals are among the early adopters of advanced surgical systems, including ultrasonic aspirators, driven by both government healthcare funding and collaborations with leading medical device manufacturers.

The Asia-Pacific ultrasonic aspirator market was valued at 18.7% market share in 2024

Asia-Pacific is projected to be the fastest-growing region in the ultrasonic aspirator market, driven by expanding healthcare infrastructure, rising cancer and neurological disease prevalence, and increasing government investments in advanced medical technologies. Growing awareness among surgeons about the clinical benefits of ultrasonic aspirators, coupled with the gradual adoption of minimally invasive surgeries, is accelerating market penetration across developing economies.

Within the Asia-Pacific, Japan holds a dominant share, as it has a highly advanced healthcare system, a strong base of neurosurgical expertise, and early adoption of precision surgical tools. Meanwhile, countries like China and India are witnessing rapid growth due to rising surgical volumes, increasing healthcare spending, and government initiatives to modernize hospitals. The combination of established markets like Japan and emerging demand from China and India is creating a dual growth engine, making Asia-Pacific the most dynamic region for future market expansion.

Competitive Landscape

The major players in the ultrasonic aspirator market include Stryker, Integra LifeSciences Corporation, Olympus Corporation, Söring GmbH, Johnson & Johnson MedTech, Nautilus Surgical, Bioventus, among others.

Stryker:

Stryker’s Sonopet series is a leading line of ultrasonic aspirators renowned for their precision, versatility, and ergonomic design in neurosurgical and orthopedic procedures. The flagship model, the Sonopet iQ, offers advanced features such as Pulse Control technology, which allows surgeons to regulate tissue resection with greater control. The system is equipped with RFID-enabled intelligence, enabling automatic adjustment of settings based on the connected tip or user profile, enhancing operational efficiency. Its

Market Scope

Metrics | Details | |

CAGR | 6.7% | |

Market Size Available for Years | 2022-2033 | |

Estimation Forecast Period | 2025-2033 | |

Revenue Units | Value (US$ Mn) | |

Segments Covered | Form | Standalone Ultrasonic Aspirator, Integrated Ultrasonic Aspirator |

Indication | Neurosurgery, Gynecological Surgery, Brain Cancers, Ischemic Stroke, Traumatic Brain Injury, Orthopedic & Spine Surgery, Others | |

Route of Administration | Hospitals, Ambulatory Surgical Centers, Specialty Clinics, Others | |

Regions Covered | North America, Europe, Asia-Pacific, South America, and the Middle East & Africa | |

The global ultrasonic aspirator market report delivers a detailed analysis with 73 key tables, more than 76 visually impactful figures, and 195 pages of expert insights, providing a complete view of the market landscape.

Suggestions for Related Report

For more medical device-related reports, please click here