Japan Pharmaceutical Secondary Packaging Market Overview

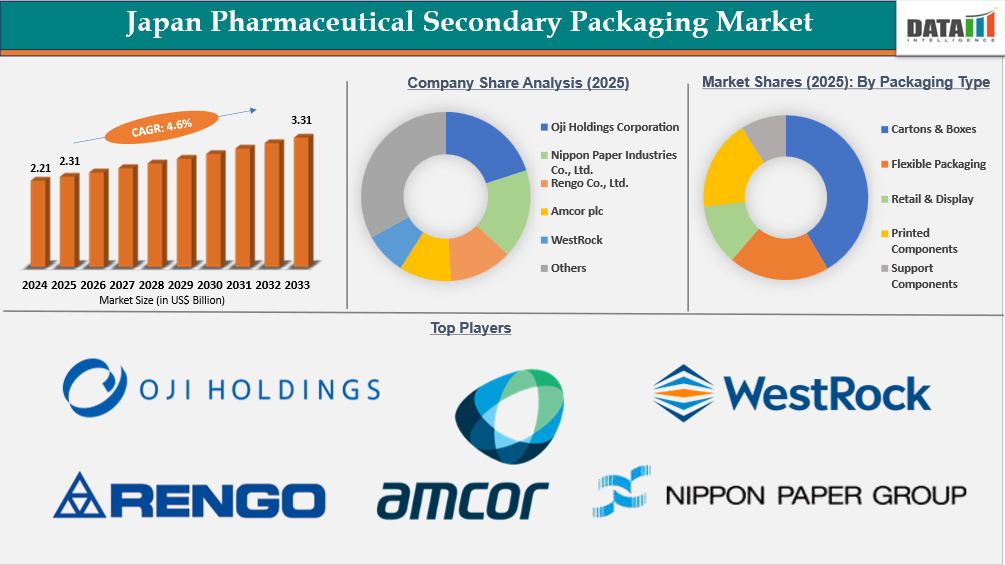

The Japan pharmaceutical secondary packaging market reached US$2.21 Billion in 2024, rising to US$2.31 Billion in 2025 and is expected to reach US$3.31 Billion by 2033, growing at a CAGR of 4.6% from 2026 to 2033.

The market is being driven largely by increased demand for secondary packaging formats such as folding cartons, printed leaflets, labels, and protective packaging components that support Japan's highly regulated pharmaceutical supply chain and quality-controlled distribution system. Secondary packaging is vital for ensuring serialization compliance, anti-counterfeiting protection, and patient information sharing, all of which are especially important under Japan's pharmaceutical regulatory system, which is controlled by PMDA regulations.

Furthermore, the Japanese pharmaceutical market structure is heavily reliant on generic pharmaceuticals, which account for around 89% of prescription volume, resulting in high-volume packaging needs for hospital and retail pharmaceutical distribution channels. Japan's highly automated pharmaceutical logistics infrastructure, as well as customer trust in high-quality packaged medications, help to drive the industry. Pharmaceutical distributors in Japan are progressively using standardized carton-based secondary packaging forms for robotic sorting, warehouse automation, and supply chain traceability. These fundamental healthcare, demographic, and regulatory reasons are likely to drive long-term growth in Japan's pharmaceutical secondary packaging industry.

Pharmaceutical Secondary Packaging Industry Trends and Strategic Insights

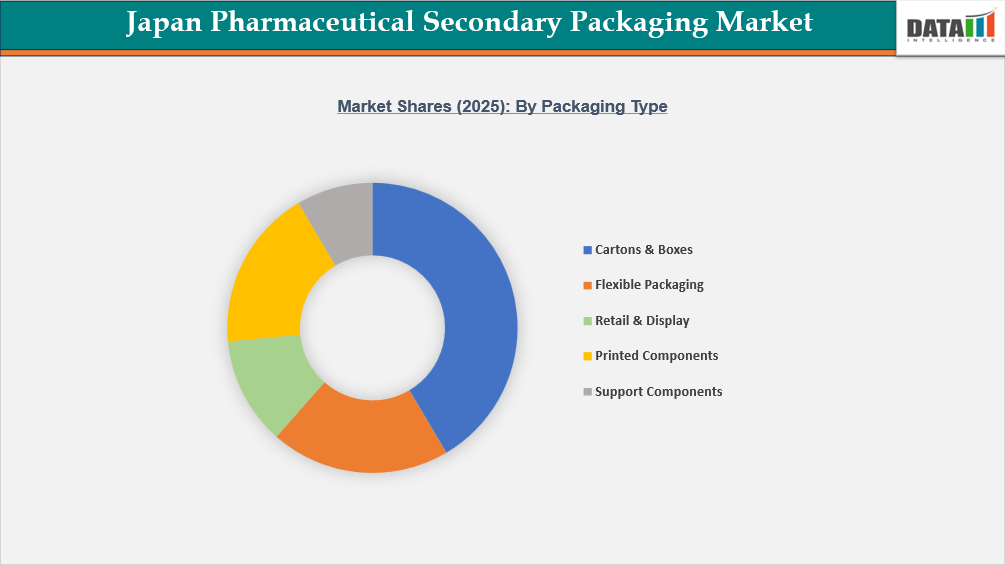

- By packaging type, cartons & boxes led the Japan pharmaceutical secondary packaging market, capturing the largest revenue share of 41.5% in 2025.

Japan Pharmaceutical Secondary Packaging Market Size and Future Outlook

- 2025 Market Size: US$2.31 Billion

- 2033 Projected Market Size: US$3.31Billion

- CAGR (2026–2033):4.6%

Market Dynamics

Growing pharmaceutical production and specialty drugs

One of the key drivers of the Japan pharmaceutical secondary packaging market is the fast expansion of pharmaceutical production, notably in specialty pharmaceuticals and high-value treatments. Japan is one of the world's major pharmaceutical markets, with specialty pharmaceuticals and biologics contributing to a growing proportion of overall medication expenditure. This increase in output immediately translates into increased demand for secondary packaging, as manufacturers seek compliant and protective package forms to accommodate the growing number of items sent domestically and internationally.

The expansion in specialty medication manufacture, such as targeted therapies, biosimilars, and advanced injectables, has increased the demand for high-performance packaging materials that maintain product integrity during distribution. For example, demand for oncology medicines in Japan has increased by an estimated 6-8% each year over the last five years, due to a rapidly aging population (with more than 28% aged 65 and over) and continuous investment in cancer treatment programs. These specialized medications frequently necessitate advanced secondary packaging with characteristics such as moisture or light barrier protection, serialization for traceability, and improved labeling for regulatory compliance.

As a result, the growing footprint of specialty pharmaceutical manufacture, which includes biologics, cancer medications, and injectable items, is a significant driver of development in Japan's secondary packaging business.

Segmentation Analysis

The Japan pharmaceutical secondary packaging market is segmented based on the packaging type, material type, end use, and functionality.

Dominance of Cartons & Boxes in the Japan Pharmaceutical Secondary Packaging Market

By packaging type, the cartons & boxes category dominates the Japan pharmaceutical secondary packaging industry, accounting for around 41.5%. This segment maintains its leadership position in Japan's pharmaceutical supply chain by striking the ideal balance between regulatory compliance, product protection, and operational efficiency. Pharmaceutical packaging must provide complete product information, including dose guidelines, adverse effects, and manufacturer data, in accordance with PMDA regulatory criteria. This crucial information may be printed in high quality on the solid surface of folding cartons, which is not possible with smaller or more flexible packing types.

Furthermore, cartons are very compatible with Japan's modern and automated logistics infrastructure. Carton packaging has standardized dimensions that are designed for high-speed sorting, warehouse automation, and robotic handling systems utilized across major pharmaceutical distribution networks. Culturally, Japanese consumers determine boxed medications with product safety, authenticity, and quality assurance, which builds brand trust and drives continuous demand for carton-based secondary packaging.

Competitive Landscape

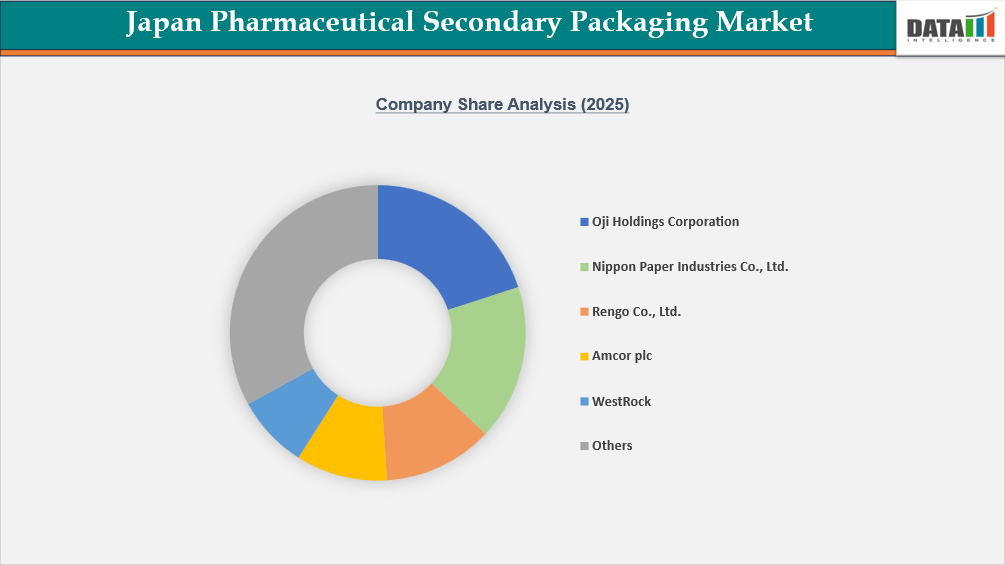

The competitive landscape of the Japanese pharmaceutical secondary packaging industry is relatively consolidated, with local packaging material makers dominating and global packaging technology suppliers participating selectively. Leading Japanese packaging companies, including Oji Holdings Corporation, Nippon Paper Industries Co., Ltd., and Rengo Co., Ltd., compete predominantly in the folding carton, printed packaging materials, pharmaceutical inserts, and corrugated protective packaging categories. To retain a strong market position, these companies use innovative printing technology, high-quality paperboard materials, and have built relationships with global pharmaceutical producers.

Amcor plc and WestRock are global packaging suppliers that compete by providing high-barrier flexible packaging materials, serialization-compatible packaging structures, and assistance for multinational pharmaceutical businesses operating in Japan. Nipro Corporation, Hosokawa Yoko Co., Ltd., Takigawa Corporation, and Mitsui Bussan Packaging Co., Ltd. compete by providing personalized pharmaceutical packaging services, regulatory-compliant packaging formats, and integrated supply chain packaging solutions. Demand for serialization compliance, anti-counterfeiting packaging features, sustainable paper-based materials, and high-quality hospital pharmaceutical supply packaging is driving market competition, supported by Japan's aging population and rising specialty drug consumption.

Key Developments

- In January 2024, Takeda Pharmaceutical Company Limited declared that it would switch from special color inks to CMYK inks for printing secondary packaging for its Japanese-made pharmaceuticals to lessen environmental impact. This effort, which aims to lower ink waste, solvent consumption, and printing-changeover waste, is set to be implemented across all relevant products by 2026.

What Sets This Japan Pharmaceutical Secondary Packaging Market Intelligence Report Apart

- Latest Data & Forecasts – Up-to-date market intelligence through 2033, covering demand by packaging type, material type, end-use, and functional performance, analyzed in terms of market value and revenue contribution.

- Regulatory Intelligence – In-depth assessment of Japan pharmaceutical regulatory frameworks impacting packaging compliance and commercialization, including PMDA, local pharmaceutical labeling standards, serialization requirements, anti-counterfeiting mandates, and post-market quality surveillance regulations.

- Competitive Benchmarking – Structured benchmarking of leading packaging manufacturers and technology providers based on product portfolio strength, innovation capabilities, sustainability initiatives, pricing strategies, and strategic partnerships within Japan’s pharmaceutical supply chain.

- Actionable Strategies & Cost Dynamics – Strategic insights into packaging lifecycle optimization, sustainability-driven material adoption, cost efficiency pressures, smart packaging integration, and advanced manufacturing capabilities, supported by perspectives from industry specialists and regulatory experts.