HVDC Transmission Market Overview

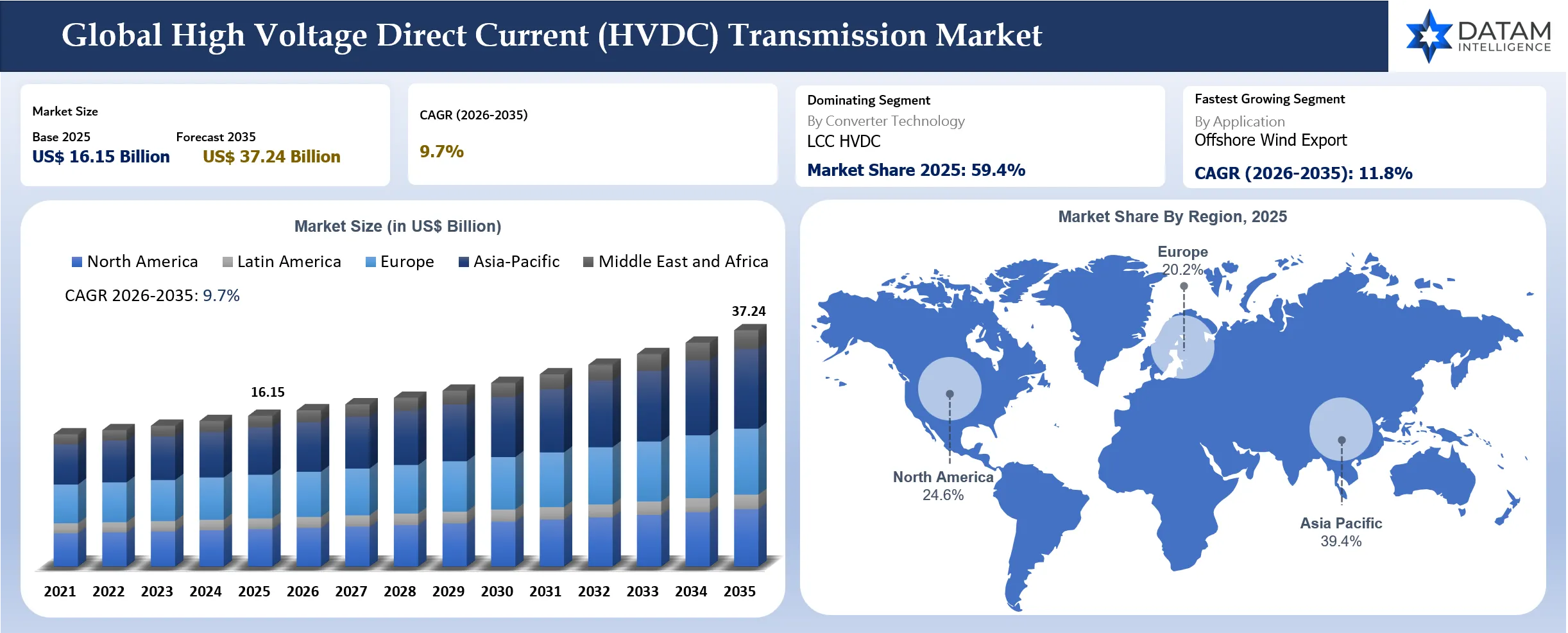

The global high voltage direct current (HVDC) transmission market reached US$ 16.15 billion in 2025 and is expected to reach US$ 37.24 billion by 2035, growing at a CAGR of 9.7% during 2026 to 2035.

Demand is being reshaped by offshore wind, cross-border power trading, long-distance renewable evacuation, grid stability requirements and rising congestion across aging AC corridors. Utilities and transmission developers are using HVDC where high-capacity power needs to move across long distances, submarine routes, underground corridors or weak-grid interfaces. VSC HVDC is gaining stronger attention for offshore wind and grid-support applications, while LCC HVDC remains commercially important for large bulk power transfer where project scale and stable grid conditions support the technology.

Europe remains the most strategically visible region because offshore wind export links, interconnectors and grid congestion are turning HVDC into a core energy-transition tool. Asia-Pacific will remain a major growth engine through China’s ultra-high-voltage build-out, india’s renewable corridors, Japan’s offshore grid needs and South Korea’s power transmission upgrades. Supplier differentiation will depend on converter station capability, cable availability, control and protection quality, project execution discipline, lifecycle service and ability to coordinate large multi-party infrastructure programs.

Market Scope

| Metrics | Details | |

| Market Size in 2025 | US$ 16.15 Billion | |

| Market Size by 2035 | US$ 37.24 Billion | |

| CAGR During 2026 to 2035 | 9.7% | |

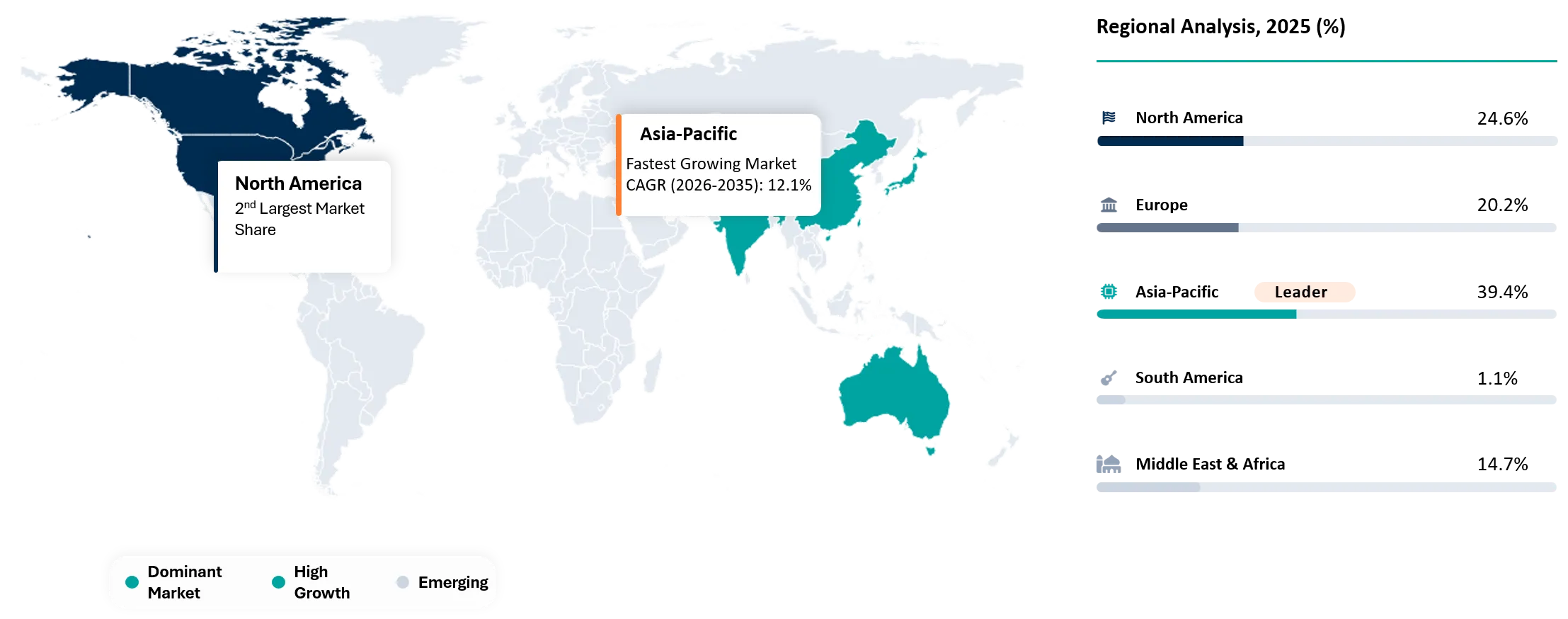

| Largest Region in 2025 | Asia-Pacific, market share 39.4% | |

| Fastest Growing Region | Asia-Pacific, CAGR 12.1% between 2026 and 2035 | |

| Leading Converter Technology | LCC HVDC | |

| Fastest Growing Converter Technology | VSC HVDC | |

| Leading Component | Converter Stations | |

| Fastest Growing Application | Offshore Wind Export | |

| Market Maturity | Growth Stage | |

| Key Buying Question | Which HVDC architecture can move more renewable power with lower congestion risk and stronger grid controllability? | |

| By Converter Technology | LCC HVDC, VSC HVDC, Hybrid HVDC, Grid Forming HVDC Platforms | |

| By Link Architecture | Point to Point, Back to Back, Multi Terminal, Offshore Hub Configurations | |

| By Component | Converter Stations, Subsea Cables, Underground Land Cables, Overhead Transmission Lines, Control and Protection Systems | |

| By Application | Renewable integration, interconnections, Bulk Power Transfer, Offshore Wind Export, Grid Stability Services | |

| By Project Environment | Onshore Corridors, Offshore Links, Cross-Border Systems, Remote Resource Evacuation | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, india, Japan, Australia, South Korea, indonesia, Malaysia | |

| South America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Key Takeaways

- HVDC transmission is becoming a strategic grid investment category as renewable power, offshore wind and interconnections create transmission requirements that conventional AC expansion cannot always solve efficiently.

- LCC HVDC will continue to dominate large bulk power transfer in regions with established high-capacity transmission corridors and stable grid connection points. LCC HVDC reached market share of 59.4% in 2025.

- VSC HVDC is expected to grow faster because offshore wind export, weak-grid renewable integration and underground cable projects require flexible control, compact stations and stronger system support.

- Converter stations remain the leading component because valves, transformers, filters, cooling systems, control platforms and protection systems define project economics and grid performance.

- Offshore wind export is the fastest-growing applications with a CAGR of 11.8% between 2026 and 2035, as Europe, China, Japan, South Korea and U.S. move toward larger offshore wind zones located farther from load centers.

- Europe remains the most visible project market due to interconnectors, offshore wind links and corridor-level grid planning, while Asia-Pacific carries the strongest long-term opportunity with a market share of 39.4% in 2025 and.

- Supplier differentiation is moving toward integrated converter and cable execution, digital protection, grid-forming control capability, lifecycle service and bankable project delivery.

Why Does This Report Matter in 2026?

HVDC transmission matters in 2026 because power systems are facing a physical grid constraint, not only a generation constraint. Renewable capacity can be built faster than long-distance transmission in many countries. Curtailment, congestion, queue delays and local opposition to overhead AC lines are making HVDC a more practical option for selected high-capacity corridors. Transmission owners increasingly need technology that can move large power blocks across difficult geographies while improving controllability.

Offshore wind is creating a second commercial trigger. Larger offshore wind projects are moving farther from shore and require export systems that can carry power efficiently to onshore grids. HVDC becomes more attractive as distance, capacity and grid stability requirements rise. Offshore hub planning and multi-terminal concepts are also pushing buyers to think beyond one-off point-to-point links.

Energy security has raised the strategic value of interconnections. Countries are using cross-border links to balance power, access renewable resources and reduce dependence on single fuel sources. Project owners need analysis that connects technology choice, permitting risk, cable availability, converter station execution and long-term grid value. A strong HVDC report must therefore evaluate project economics, supply constraints and policy momentum together.

Strategic indicators For HVDC Transmission

High Regulation Impact

HVDC projects are shaped by grid codes, energy policy, seabed permitting, land rights, environmental approvals, offshore wind connection rules and cross-border regulatory frameworks. A single project may require alignment among transmission system operators, energy regulators, marine authorities, local communities and environmental agencies. Regulatory complexity can materially affect schedule, cost and supplier selection.

Europe shows the clearest regulatory influence because offshore grid planning and interconnector approval are tied to climate targets and energy security. Projects must pass cost-benefit review, environmental assessment and route consultation before major construction can begin. Delays in one approval step can shift commissioning timelines by years.

Asia-Pacific projects also face route and land challenges. China can execute large corridors at scale, while india, Japan and South Korea require more coordination around land use, offshore routes and grid integration. Regulatory readiness is therefore a major differentiator across regions.

High investment Activity

investment activity is strongest in offshore wind export links, cross-border interconnectors, renewable evacuation corridors and converter station capacity. Transmission owners are planning larger projects because renewable generation is increasingly located far from demand centers. HVDC is now part of strategic grid expansion rather than a niche technology choice.

Cable and converter capacity is attracting investment because project pipelines are larger than the historic supplier base. Large offshore links require specialized cable vessels, converter transformers, valves and control systems. Buyers are increasingly assessing supplier backlog and manufacturing footprint during procurement.

investment is also moving toward digital control and grid-forming capabilities. Future HVDC systems need to support weaker grids and higher inverter-based generation. Suppliers able to integrate hardware with advanced control systems will be better positioned for premium projects.

Supply Chain Disruption

Supply-chain disruption is a major issue because HVDC projects require specialized components with limited supplier depth. Converter transformers, valves, HVDC cables, cable installation vessels, control platforms and protection systems all have long lead times. Large projects can compete for the same engineering and manufacturing slots.

Cable availability is one of the strongest bottlenecks. Subsea and underground HVDC cables require specialized factories and vessels. Offshore wind and interconnector projects are expanding faster than cable supply capacity in several regions. Contracting early is becoming a strategic necessity.

Execution risk also comes from project interfaces. Converter suppliers, cable suppliers, civil contractors, marine installers and grid operators must align schedules and technical responsibilities. Weak coordination can delay commissioning even when individual equipment is available.

Pricing Volatility

HVDC project pricing is affected by copper, aluminum, steel, semiconductor devices, transformer materials, cable insulation, marine installation cost, civil works and engineering scope. Large projects are exposed to commodity movement and supplier capacity constraints. Fixed-price contracts can become difficult when project approval cycles are long.

Converter station cost depends on technology, voltage level, capacity, land requirements, filters, transformers, cooling and control systems. VSC platforms may command higher value in offshore and weak-grid applications because system functionality is broader. LCC systems can remain cost-effective for high-capacity bulk transfer.

Cable cost depends on route length, seabed conditions, burial depth, protection requirements and installation vessels. Marine conditions can affect installation windows and contingency cost. Buyers increasingly evaluate total project risk rather than only equipment price.

Procurement Pressure

Procurement teams are under pressure to secure capacity before final approval risk is fully cleared. HVDC projects often take years from concept to commissioning. Waiting too long can increase exposure to cable vessel shortages, transformer lead times and converter supplier backlog. Early framework agreements are becoming more common.

Technical procurement is also more complex. Buyers must compare LCC, VSC, hybrid architectures, cable routes, converter station design, losses, fault response and operational flexibility. Lowest upfront price may not deliver the best system value if grid support, controllability or expansion potential is weak.

Supplier bankability is central. Transmission developers prefer vendors that can deliver large programs, manage interfaces and support long operating lives. Warranty, lifecycle service and digital monitoring are becoming part of procurement evaluation.

New Technology Adoption

Technology adoption is strongest in VSC HVDC, grid-forming controls, digital protection, offshore hubs, multi-terminal planning and digital twin support. VSC systems support offshore wind, underground routes and weak-grid connections because active and reactive power can be controlled more flexibly.

Grid-forming HVDC platforms are gaining attention because power systems are adding more inverter-based resources. Transmission operators need technologies that can support stability when synchronous generation declines. Control architecture will become a stronger differentiator.

Digital twins and monitoring platforms are also becoming more relevant. HVDC assets are long-life infrastructure with high availability requirements. Operators want better visibility into converter health, cable condition, control behavior and maintenance planning.

Import-Export Scenario

HVDC import-export tracking should focus on converter equipment, high-voltage cables, power transformers, switchgear and control panels. Trade flows cannot isolate a complete HVDC project through one code, but selected codes help identify the movement of critical equipment and project supply-chain pressure.

| HS Code | Trade Item | Import-Export Relevance |

| 850440 | Static Converters | indicates converter equipment movement linked to HVDC stations, power electronics and grid interface systems |

| 854460 | Electric Conductors Above 1,000 V | Tracks high-voltage cable trade relevant to land and subsea HVDC links |

| 850423 | Liquid Dielectric Transformers Above 10,000 kVA | Supports review of converter transformer and high-voltage transformer trade |

| 853720 | Boards Panels and Consoles Above 1,000 V | Captures high-voltage control and protection panels used in transmission systems |

| 853530 | Isolating Switches and Make-and-Break Switches Above 1,000 V | indicates trade in high-voltage switching equipment used in converter stations |

| 854690 | Electrical insulators Other Than Glass or Ceramic | Supports evaluation of high-voltage insulation components used in transmission infrastructure |

AI Impact Analysis

AI can improve HVDC planning by supporting route analysis, failure risk evaluation, maintenance scheduling and grid simulation. Transmission projects generate large datasets across terrain, weather, seabed conditions, load flow, converter behavior and outage risk. AI tools can help planners evaluate project alternatives faster and identify risk points earlier.

AI can also improve operation and maintenance. Converter stations, cables and control systems require high availability. Predictive models can monitor temperature, vibration, partial discharge signals, control anomalies and component aging. Better diagnostics can reduce unplanned outages and support maintenance scheduling.

AI will have the strongest value when connected to engineering workflows rather than presented as an isolated dashboard. Grid operators need explainable recommendations because transmission assets are safety-critical. AI adoption will therefore favor tools that support human engineers and provide auditable decision logic.

Disruption Analysis

Offshore grid planning is disrupting the HVDC market because future projects may not remain simple point-to-point links. Offshore hubs, multi-terminal systems and cross-border wind corridors are increasing system complexity. Suppliers must prepare for projects where converter controls, protection systems and interoperability matter as much as hardware rating.

Cable supply constraints are also disrupting project development. A strong project pipeline can still face delays when cable factories and installation vessels are booked years ahead. Developers increasingly need procurement strategies that lock supply early and reduce interface risk.

Grid-forming control is changing competitive positioning. Transmission owners need HVDC systems that can support stability in grids with high renewable penetration. Suppliers with advanced control and protection platforms can differentiate beyond standard converter capacity.

BCG Matrix: Company Evaluation

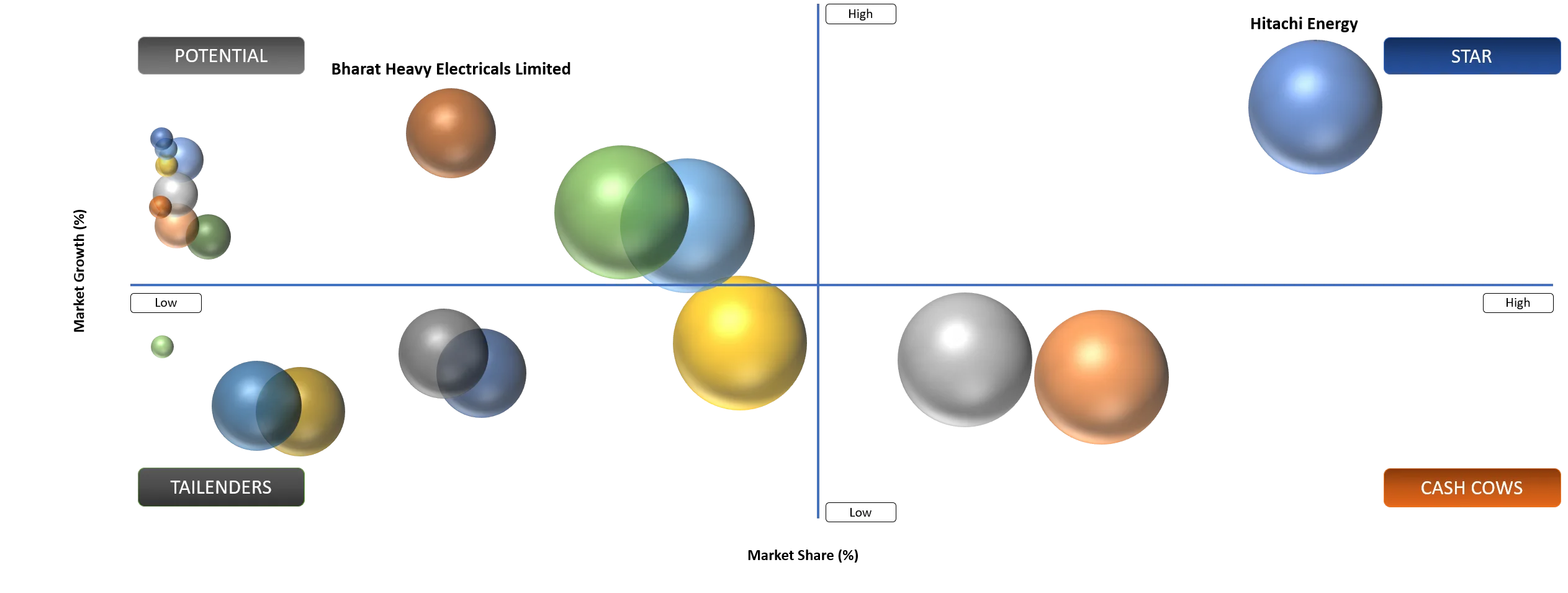

Star

Star players include Hitachi Energy Ltd., Siemens Energy AG, GE Vernova inc., Prysmian S.p.A., Nexans S.A. and NKT A S. These companies have strong technical credibility, project references, manufacturing capacity and relevance across converters, cables or large-scale transmission execution. Leadership depends on project delivery, lifecycle support and ability to serve high-value offshore and interconnector programs.

Potential

Potential companies include NR Electric Co., Ltd., Bharat Heavy Electricals Limited and RONGXIN POWER ELECTRONIC CO., LTD. These companies can gain share through regional grid investment, localized supply, power electronics specialization and participation in renewable transmission programs. Movement into the strongest leadership tier will depend on international validation, project scale and long-term service credibility.

Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact | Demand Concentration | Impacted Application | Strategic Impact |

Offshore Wind and Weak-Grid Renewable integration Push Utilities toward VSC HVDC | High | Europe, China, Japan and South Korea | Offshore Wind Export | Drives converter station and subsea cable demand |

Cross-Border interconnection Plans Expand Around Energy Security | High | Europe and Middle East | interconnections | Supports long-distance power exchange |

Transmission Congestion Makes HVDC Attractive Where AC Expansion Is Land intensive | Medium to High | North America, Europe and india | Bulk Power Transfer | Improves corridor utilization and reduces curtailment |

Offshore Wind and Weak-Grid Renewable integration Push Utilities toward VSC HVDC

Offshore wind is one of the strongest HVDC demand drivers because project distance and capacity are increasing. Long export routes create losses and stability issues when conventional AC systems are used over long submarine distances. VSC HVDC helps move power efficiently while offering control features that support offshore integration.

Weak-grid renewable connections are also pushing demand. Solar, wind and hydro resources are often located far from load centers and may connect into networks with limited stability. HVDC can support power transfer while improving controllability. Grid-forming functions will become increasingly important as inverter-based generation grows.

Utilities also value corridor efficiency. HVDC can move large power blocks through narrower routes than comparable AC expansion. This matters where land acquisition, public opposition or environmental constraints delay conventional transmission development.

Restraint Impact Analysis

| Restraint | Drag On Market Growth | Primary Impact Area | Impacted Application | Strategic Impact |

Permitting Route Studies and Cable Availability Keep Project Cycles Long | High | Offshore and Onshore Corridors | interconnections and Offshore Wind Export | Delays final investment and commissioning |

Concentrated Supply Base For Cables Valves and Control Systems Raises Execution Risk | High | Critical Components | Converter Stations and Subsea Links | increases procurement urgency |

Public Acceptance For Land Routes and Coastal Landing Sites Remains Difficult | Medium | Project Development | Underground and Subsea Links | Raises consultation and redesign cost |

Permitting Route Studies and Cable Availability Keep Project Cycles Long

HVDC projects require extensive permitting and stakeholder coordination. Offshore cable routes need seabed surveys, marine consent and landing approvals. Onshore corridors require land rights, environmental studies and community engagement. Approval delays can shift commissioning schedules and create cost escalation.

Cable availability is another major restraint. Specialized HVDC cables and installation vessels have limited capacity. Offshore wind and interconnector projects compete for the same supply base. Developers that do not secure cable capacity early can face delays even after regulatory approval.

Converter station design also adds complexity. Land availability, grid connection, cooling, transformers, filters and control systems must be coordinated with local network conditions. Suppliers with strong project engineering can reduce risk, but approval and execution cycles remain long.

Segmentation Analysis

VSC HVDC Will Capture The Fastest Growth in Offshore and Weak-Grid Use Cases

VSC HVDC is expected to grow fastest because it supports offshore wind, underground routes, weak-grid renewable integration and compact station designs. VSC platforms provide flexible control of active and reactive power, which is valuable where grid stability and renewable intermittency are major concerns.

Offshore wind export is the strongest use case. Wind farms located far from shore need efficient export links and stable grid connection. VSC HVDC offers better suitability for offshore converter platforms and long submarine cable routes. As offshore projects scale, VSC demand will expand.

VSC also supports urban and underground applications. Dense cities and constrained corridors often require cable-based transmission rather than overhead AC expansion. Compact converter stations and controllability make VSC attractive where space and public acceptance matter.

LCC HVDC Will Remain Important For Bulk Power Transfer

LCC HVDC will continue to dominate very large bulk power transfer where stable AC systems and long-distance corridors are available. China, india and selected long-distance transmission markets still rely on LCC for high-capacity power movement. The technology is proven and efficient for large point-to-point projects.

LCC systems are best suited where the receiving and sending grids are strong enough to support commutation. Large hydro, coal, wind and solar evacuation corridors can use LCC when system conditions align. Project economics remain attractive at very high power ratings. LCC growth may be slower than VSC in offshore and weak-grid applications, but installed base and large-scale project relevance remain high. Suppliers with expertise in both LCC and VSC can serve broader demand.

Converter Stations Will Remain The Highest-Value Component

Converter stations remain the highest-value component because they contain valves, transformers, control systems, filters, cooling, protection and grid interface equipment. Station design determines performance, losses, reliability and operational flexibility. Buyers evaluate converter partners carefully because failure risk is high.

Control and protection systems are gaining importance. Future grids require faster fault response and stronger interoperability. Digital control platforms can differentiate suppliers and create lifecycle service opportunities. Subsea and underground cables also represent a critical growth component. Offshore wind and interconnector projects require long cable routes and specialized installation. Cable suppliers will hold stronger negotiating power as project pipelines expand.

Market Segmentation

- By Converter Technology

- LCC HVDC

- VSC HVDC

- Hybrid HVDC

- Grid Forming HVDC Platforms

- By Link Architecture

- Point to Point

- Back to Back

- Multi Terminal

- Offshore Hub Configurations

- By Component

- Converter Stations

- Subsea Cables

- Underground Land Cables

- Overhead Transmission Lines

- Control and Protection Systems

- By Project Environment

- Onshore Corridors

- Offshore Links

- Cross-Border Systems

- Remote Resource Evacuation

- By Application

- Renewable integration

- interconnections

- Bulk Power Transfer

- Offshore Wind Export

- Grid Stability Services

Geographical Penetration

Europe HVDC Transmission Market Growth Trends

Europe remains the most commercially visible HVDC region because offshore wind, interconnectors and grid congestion are major policy priorities. The North Sea, Baltic Sea and UK power corridors are creating demand for subsea links, offshore hubs and converter stations. Energy security concerns have also increased support for cross-border interconnection.

Germany is central because renewable integration and north-south grid constraints require major transmission reinforcement. Underground HVDC corridors are important because public acceptance for overhead lines remains difficult. Buyers value project execution, route planning and supplier capacity.

UK demand is shaped by offshore wind export and Scotland-to-England grid reinforcement. Large subsea HVDC projects support renewable transfer to demand centers. Developers need cable supply, converter stations and coordinated regulatory approvals. Norway, Denmark, Netherlands and Sweden support interconnector and offshore grid opportunities. Regional power trading and offshore wind planning make HVDC a strategic infrastructure category. Suppliers with European project execution capability will remain well positioned.

Asia-Pacific HVDC Transmission Market Expansion Outlook

Asia-Pacific carries the strongest long-term volume opportunity. China remains the global benchmark for large-scale long-distance HVDC deployment. Renewable evacuation, west-to-east power transfer and ultra-high-voltage projects support sustained demand.

india is expanding renewable transmission corridors to move solar and wind power from resource-rich states to demand centers. HVDC can help reduce congestion and support bulk transfer where AC corridors face land and stability limitations. Domestic manufacturing and localized project execution will be important.

Japan and South Korea are emerging offshore wind and grid reinforcement markets. Island geographies, offshore resources and constrained grid corridors increase the value of cable-based HVDC solutions. Project timing will depend on policy support, permitting and transmission planning. Australia also offers opportunities linked to renewable zones and long-distance grid reinforcement. Remote resource evacuation can support HVDC feasibility where high-capacity corridors are needed.

U.S. HVDC Transmission Market Demand Analysis

The U.S. has strong HVDC potential due to renewable energy zones, offshore wind plans, transmission congestion and regional grid fragmentation. Large renewable resources are often located far from demand centers. HVDC can help move power across long distances and connect asynchronous regions.

Offshore wind delays have slowed some near-term projects, but long-term coastal grid reinforcement remains important. Atlantic offshore wind export, Gulf Coast industrial power needs and western renewable corridors can support future HVDC demand. Permitting remains the biggest challenge. interregional transmission is a major opportunity. Better links between grid regions can improve resilience, reduce congestion and support renewable balancing. HVDC is attractive where long-distance transfer and controllability are valuable.

india HVDC Transmission Market Growth Opportunities

india is one of the strongest growth markets because renewable capacity is expanding quickly while grid reinforcement must catch up. Solar and wind resources are concentrated in states far from major demand centers. HVDC can support long-distance evacuation and reduce congestion.

Domestic suppliers and public-sector utilities play a large role. Bharat Heavy Electricals Limited, KEC international Limited and local transmission contractors can support project execution, while global converter and cable suppliers provide advanced technology. Permitting and route acquisition remain key issues. HVDC projects need coordinated planning across states, utilities and regulators. Suppliers that combine technology with local execution support will be better positioned.

Competitive Landscape

- Competition is split between converter technology leaders, cable manufacturers, grid equipment suppliers, EPC contractors and lifecycle service providers.

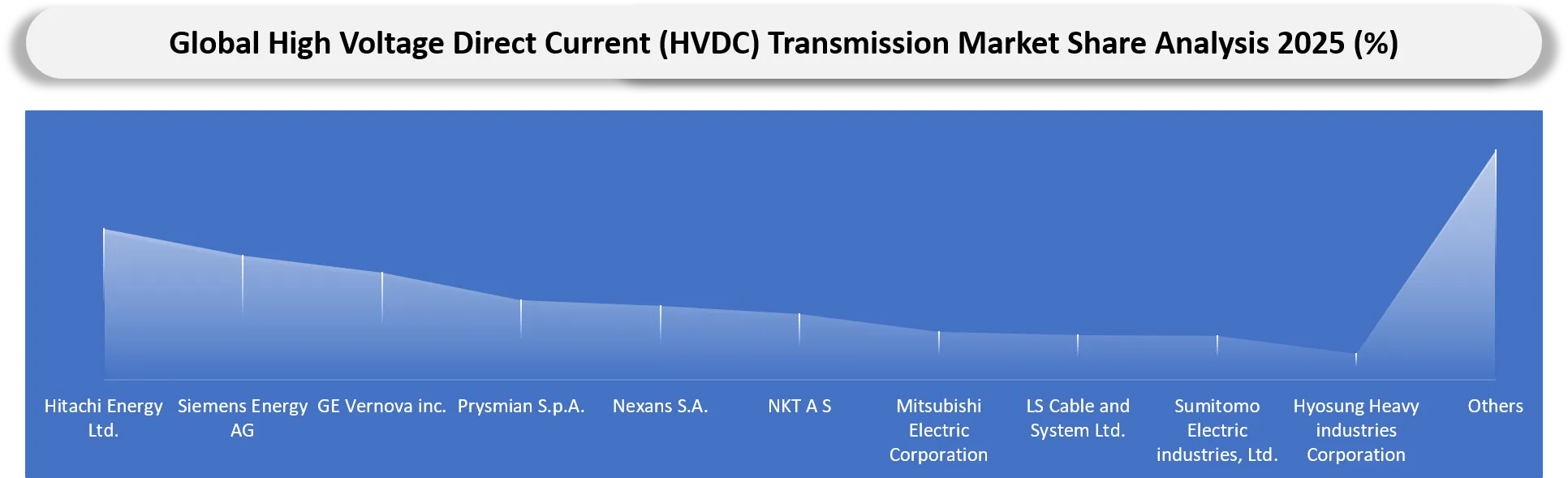

- Hitachi Energy, Siemens Energy and GE Vernova compete strongly in converter stations, control systems and high-voltage grid integration.

- Prysmian, Nexans, NKT, LS Cable and System and Sumitomo Electric compete in high-voltage cable systems where availability and installation capability are decisive.

- Regional players such as TBEA, NR Electric, BHEL, China XD Group and RONGXIN POWER ELECTRONIC can gain share through domestic transmission programs and localized supply.

- Competitive benchmarking should track converter technology coverage, cable backlog, project references, execution capacity, digital control platforms, lifecycle service and ability to manage multi-party project interfaces.

List of Companies

- Hitachi Energy Ltd.

- Siemens Energy AG

- GE Vernova inc.

- Prysmian S.p.A.

- Nexans S.A.

- NKT A S

- Mitsubishi Electric Corporation

- LS Cable and System Ltd.

- Sumitomo Electric industries, Ltd.

- Hyosung Heavy industries Corporation

- NR Electric Co., Ltd.

- toshiba Energy Systems and Solutions Corporation

- Bharat Heavy Electricals Limited

- TBEA Co., Ltd.

- KEC international Limited

- Quanta Services, inc.

- Mitsubishi Electric Power Products, inc.

- China XD Group Co., Ltd.

- RONGXIN POWER ELECTRONIC CO., LTD.

- RTE international

Company Coverage Preview

Hitachi Energy Ltd. remains one of the leading HVDC suppliers through its HVDC Light, HVDC Classic, MACH control and protection system and lifecycle service capability. The company is well positioned where offshore wind, grid stability and interconnections require converter expertise and project execution depth. Its strength comes from long HVDC history, broad technology coverage and ability to support both new systems and upgrades.

Siemens Energy AG is a major competitor across HVDC converter systems, grid technology and large-scale transmission infrastructure. The company is relevant in offshore wind export, interconnectors and grid expansion programs where utilities need high-voltage system integration. Siemens Energy benefits from engineering depth, European project exposure and grid infrastructure relationships.

GE Vernova inc., Prysmian S.p.A., Nexans S.A., NKT A S, Mitsubishi Electric Corporation, LS Cable and System Ltd. and Sumitomo Electric industries, Ltd. hold important positions across converters, cables and high-voltage transmission supply. Cable suppliers are becoming more strategically important because offshore wind and interconnector pipelines are placing pressure on high-voltage cable capacity.

Major Pain Points

- Cable and converter equipment lead times can delay project execution.

- Route permitting and public consultation can extend project cycles.

- Offshore landing sites can create environmental and community resistance.

- Multi-terminal protection remains technically complex.

- Converter station land requirements can be difficult in dense areas.

- Suppliers face high working-capital exposure on large projects.

- Grid operators need better visibility into lifecycle performance.

- Project interfaces between cable suppliers, converter vendors and civil contractors create execution risk.

- Skilled HVDC engineering talent remains limited.

- Cross-border projects need regulatory alignment between multiple markets.

Recent Developments

- March 2026: NKT signed a major HVDC cable contract linked to the UK Eastern Green Link 3 project, reinforcing high-voltage cable supply pressure in Europe’s offshore and interconnector pipeline.

- February 2026: Prysmian advanced its position in UK offshore grid reinforcement through a major Eastern Green Link 4 HVDC cable award, strengthening its role in large subsea transmission corridors.

- December 2025: GE Vernova T and D india secured a major HVDC project in india, highlighting domestic demand for high-capacity renewable transmission and grid modernization.

- October 2025: GE Vernova reported strong electrification order momentum, with grid equipment and HVDC-related demand supporting the company’s transmission infrastructure outlook.

- June 2025: Hitachi Energy india highlighted HVDC as a core technology for renewable integration and transmission modernization in india’s energy transition.

Analyst View and Opinion

- HVDC will remain one of the most strategic grid infrastructure markets because renewable generation is increasingly located far from demand centers.

- VSC HVDC will grow faster than LCC because offshore wind, underground routes and weak-grid connections need flexible control.

- LCC HVDC will remain essential for very large bulk transfer corridors where grid conditions support the technology.

- Converter stations and cables will define project bottlenecks because supplier capacity is concentrated.

- Europe will remain the most visible premium project market due to offshore wind and interconnector activity.

- Asia-Pacific will deliver the strongest long-term volume growth through China, india, Japan and South Korea.

- Grid-forming controls will become a more important differentiator as inverter-based generation rises.

- Public acceptance and permitting will remain as important as technology selection.

- Supplier advantage will shift toward execution certainty, early capacity reservation and lifecycle service.

- Multi-terminal HVDC will create a higher-value opportunity, but interoperability and protection challenges must be solved.

Target Audience

| industry | Who Should Buy This Report? | Reason to Buy This Report |

| Transmission System Operators | Grid Planning Teams, Asset Managers, Procurement Leaders | Evaluate HVDC technology choices, supplier capacity and corridor planning |

| Offshore Wind Developers | Grid Connection Teams, Project Directors | Assess export link design, converter selection and cable supply risk |

| Utilities | Strategy Teams, Grid Modernization Leaders | Track long-distance transmission and renewable integration opportunities |

| EPC Contractors | Project Development Teams, Commercial Teams | Identify project pipeline and supplier partnership opportunities |

| Cable Manufacturers | Strategy Teams, Sales Leaders | Assess high-voltage cable demand and regional project pipelines |

| Converter Equipment Suppliers | Product Teams, Business Development Teams | Track VSC, LCC and control system opportunities |

| investors | infrastructure Funds, Energy investors | Evaluate transmission bottlenecks and long-term capital deployment |

| Consulting Firms | Energy Advisory Teams | Support policy, market entry and project feasibility work |

What DataM Uniquely Provides

- DataM maps HVDC demand by converter technology, link architecture, component, application, project environment and region.

- DataM separates offshore wind export demand from interconnection, bulk transfer and grid stability use cases.

- DataM benchmarks suppliers across converter technology, cable capability, project execution and lifecycle service.

- DataM evaluates procurement risk around cable availability, converter capacity, permitting and project interfaces.

- DataM connects country-level policy, offshore wind pipelines and renewable congestion to HVDC demand formation.

- DataM identifies white-space opportunities in multi-terminal systems, grid-forming controls and offshore hubs.

- DataM provides import-export indicators for converter equipment, high-voltage cables, transformers and control panels.