Fungicides Market Size

The Fungicides Market is estimated to reach USD 26.20 Billion in 2026 and is projected to grow to USD 46.27 Billion by 2035, registering steady growth at a CAGR of 6.5% during the forecast period from 2026 to 2035.

Fungicides are chemical compounds used to kill or prevent fungi's growth, including dithiocarbamates, benzimidazoles, triazoles, strobilurins, and carboxamides. Biological fungicides are living organisms or their derivatives that can control fungal diseases, and they contribute to the Global Fungicides Market Size.

Contact fungicides are applied directly to the plant's surface, while the plant absorbs systemic fungicides and provides protection throughout the tissue, resulting in lucrative sales in the fungicide market revenue. In addition, protective fungicides create a barrier on the plant's surface to prevent fungal spores from germinating and infecting the plant, and these products also have significant sales in the global fungicides market revenue.

Fungicides Market Scope

| Metrics | Details |

| CAGR | 6.5% |

| Size Available for Years | 2023-2035 |

| Forecast Period | 2026-2035 |

| Data Availability | Value (US$) |

| Segments Covered | Origin, Mode of Application, Form, Product, Crop Type and Region |

| Regions Covered | North America, Europe, Asia-Pacific, South America and Middle East & Africa |

| Fastest Growing Region | Europe |

| Largest Region | Asia-Pacific |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth, Demand, Recent Developments, Mergers and Acquisitions, New Product Launches, Growth Strategies, Revenue Analysis, Porter’s Analysis, Pricing Analysis, Regulatory Analysis, Supply-Chain Analysis and Other key Insights. |

For More Insights about the Market Request free Sample

Key Takeaways

- The global fungicides market is witnessing steady growth driven by rising food demand, increasing crop losses due to fungal diseases, and expansion of commercial agriculture worldwide.

- Chemical fungicides continue to dominate the market due to their high effectiveness, fast action, and widespread adoption in large-scale farming systems.

- Cereals and grains represent the largest application segment, as staple crops such as wheat, rice, and corn require continuous protection from fungal infections to ensure global food security.

- Liquid formulations are gaining strong traction due to ease of application, better coverage, and compatibility with modern spraying technologies and precision agriculture systems.

- Asia-Pacific leads the market owing to extensive agricultural activity, high dependency on crop yields, and increasing adoption of modern crop protection solutions.

- Rising climate variability is increasing the incidence of crop diseases, further strengthening long-term demand for fungicide products.

- Growing shift toward biological fungicides and sustainable crop protection solutions is reshaping innovation strategies across agrochemical companies.

Analyst Viewpoint

The fungicides market is evolving from a traditional chemical input segment into a more technology-driven and sustainability-focused crop protection industry. While conventional chemical fungicides remain dominant, the market is increasingly influenced by regulatory pressure, environmental concerns, and consumer demand for residue-free food products.

A key structural driver is the rising intensity and unpredictability of crop diseases caused by climate change, which is increasing dependency on preventive crop protection strategies. This is particularly important for staple crops where yield losses directly impact global food security.

Another major transformation is the shift toward integrated pest management (IPM) and precision agriculture, where fungicides are applied in a more targeted, data-driven manner using sensors, forecasting systems, and drone-based monitoring.

In the long term, the market is expected to transition toward a hybrid model combining chemical + biological fungicides, with companies investing heavily in bio-based solutions, resistance management technologies, and sustainable crop protection platforms.

Market Dynamics

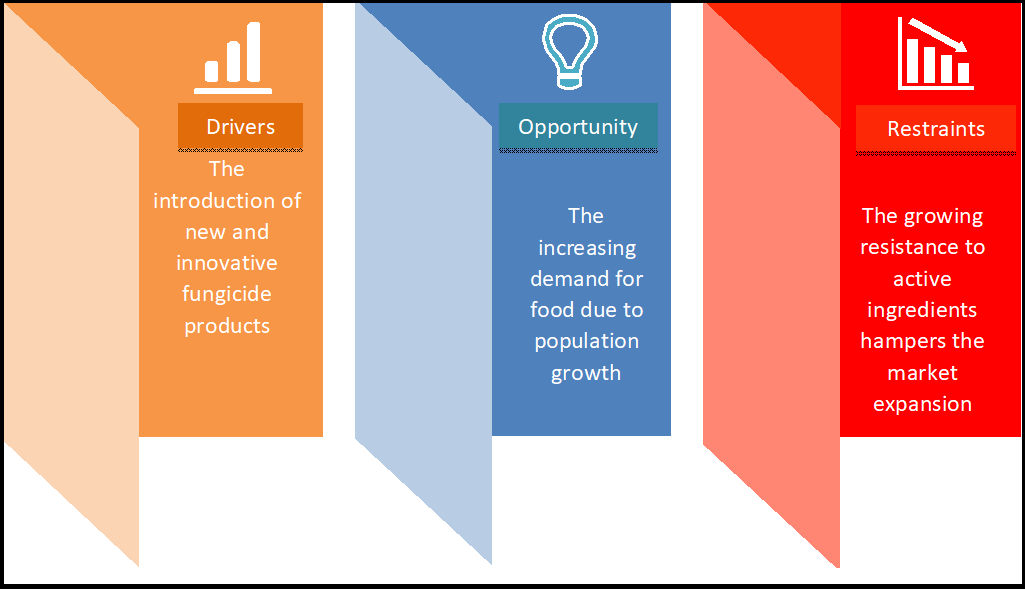

The Introduction of New and Innovative Fungicide Products

The cultivation of fruits and vegetables is expanding in response to changes in global food structures and cropping patterns, leading to a growing demand for fungicides with innovative active ingredients. For instance, on November 10, 2022, FMC Corporation launched three modes of action foliar fungicide targeting late-season diseases – adastri fungicide.

In addition, FMC Corporation's fluindapyr, was approved by the U.S. Environmental Protection Agency in 2021 for use in specialty crops and turfs. With strobilurin fungicides facing increasing disease resistance, manufacturers are prioritizing the development of strobilurin-based products in combination with other ingredients to improve efficacy and overcome resistance challenges.

Fungicides Market Segment Analysis

The Global Fungicides Market is segmented based on origin, mode of application, form, product, crop type, and region.

Grains & Cereals Segment Accounts for the Highest Share in Global Fungicides Market

The consumption of fungicide products is highest in the grains & cereals segment, which can be attributed to their increased application rate per hectare and the large areas harvested for crops such as corn, wheat, and rice - staple food items in regions such as America, Europe, and Asia-Pacific.

As the demand for these cereal crops increases, so does the need for fungal pesticide products that protect against diseases and pests. For instance, The Food and Agriculture Organization (FAO) reported a total production of 8358190.79 tons of cereals in 2021, highlighting the need for innovative fungicidal crop protection products.

Market Geographical Share

Asia-Pacific is the Dominating Region During the Forecast Period.

By region, the Global Fungicides Market is segmented into North America, South America, Europe, Asia-Pacific, Middle-East and Africa.

However, governments in these countries are encouraging modern farming, in which farmers are educated on various factors such as chemical usage, crop type, soil conditions, and periodic application of fungicides. This approach is expected to significantly impact crop output with lower investment.

Market Companies

The major global players include BASF SE, ADAMA Agricultural Solutions Ltd., Bayer CropScience AG, DuPont, FMC Corporation, Monsanto Company, Nufarm Limited, Sumitomo Chemical Co., Ltd, Syngenta AG and The DOW Chemical Company.

Key Developments

- June 2026 – Bayer CropScience and BASF expanding next-generation crop protection solutions

Bayer CropScience AG and BASF SE advanced development of broad-spectrum fungicides with improved resistance management and longer residual protection for major row and specialty crops. - May 2026 – Syngenta and FMC strengthening sustainable fungicide portfolios

Syngenta AG and FMC Corporation expanded bio-enhanced and low-residue fungicide formulations designed to improve crop yield protection while supporting stricter global residue regulations. - April 2026 – Sumitomo Chemical and ADAMA advancing integrated disease management solutions

Sumitomo Chemical Co., Ltd. and ADAMA Agricultural Solutions Ltd. enhanced fungicide combinations and crop protection programs aimed at improving effectiveness against resistant fungal strains. - April–June 2026 – Rising demand for resistance management and sustainable agriculture inputs

Companies such as Nufarm Limited, Monsanto Company, DuPont, and Dow Chemical expanded R&D efforts in advanced fungicide chemistry, biological integration, and precision application technologies to support sustainable farming practices.

Investment Hotspots & White Space Opportunities

The fungicides industry is attracting strong investment due to rising food demand, climate risks, and sustainable agriculture transitions.

High-Growth Investment Areas

• Chemical fungicides with improved efficacy and lower toxicity

• Biofungicides and microbial-based crop protection solutions

• Seed treatment fungicide technologies

• Liquid formulation innovations for precision spraying

• Foliar spray optimization systems

• Combination fungicide products (multi-mode action)

• Digital agriculture integration platforms

White Space Opportunities

• AI-based crop disease prediction and fungicide optimization

• Nanotechnology-based fungicide delivery systems

• Climate-resilient crop protection formulations

• Fully biological, residue-free fungicide systems

• Drone-based autonomous fungicide application systems

• Resistance management and smart rotation systems

• Soil microbiome-friendly fungicide solutions

• Sustainable “zero-residue export agriculture” solutions

Companies investing early in biological innovation and precision agriculture integration are expected to gain long-term competitive advantage as regulatory pressure increases.

Who Should Purchase This Report & Why

Agrochemical Companies

To understand demand trends, product innovation opportunities, and competitive positioning.

Crop Protection Manufacturers

To evaluate chemical vs biological fungicide growth and future portfolio strategies.

Agricultural Producers & Farming Cooperatives

To optimize crop protection strategies and improve yield efficiency.

Seed Companies

To assess seed treatment fungicide demand and early-stage crop protection technologies.

Food & Agribusiness Companies

To ensure supply chain stability and reduce crop loss risks across sourcing regions.

Private Equity & Institutional Investors

To identify high-growth opportunities in agrochemicals, bio-based crop protection, and precision agriculture.

Government & Agricultural Policy Bodies

To evaluate food security risks and sustainable farming practices.

Consulting & Strategy Firms

To support market entry, acquisition analysis, and agrochemical industry forecasting.

The Global Fungicides Market Report Would Provide Approximately 77 Tables, 82 Figures, And 195 Pages.

Target Audience

- Manufacturers/ Buyers

- Industry Investors/Investment Bankers

- Research Professionals

- Emerging Companies