Bispecific Antibodies in Precision Oncology Market Overview

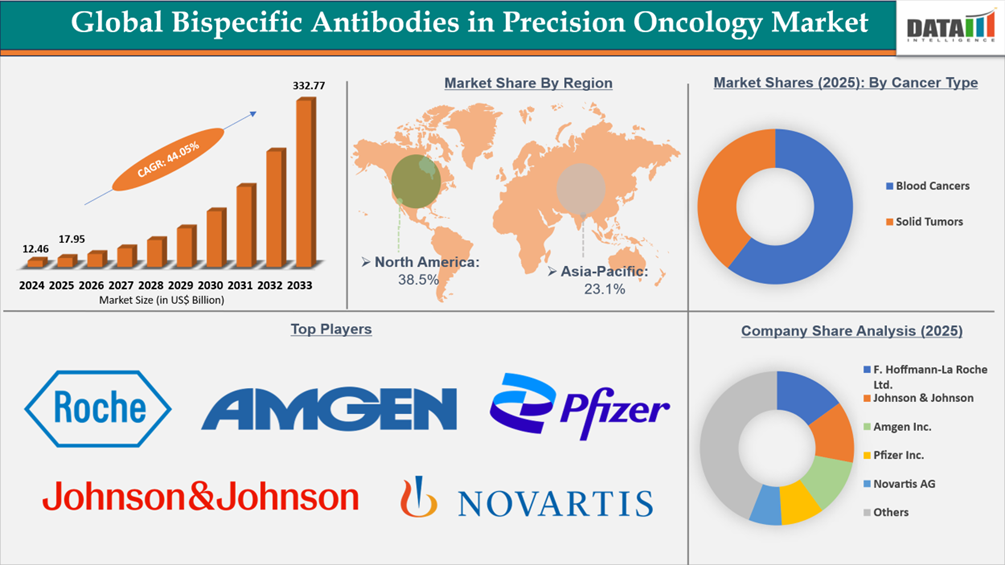

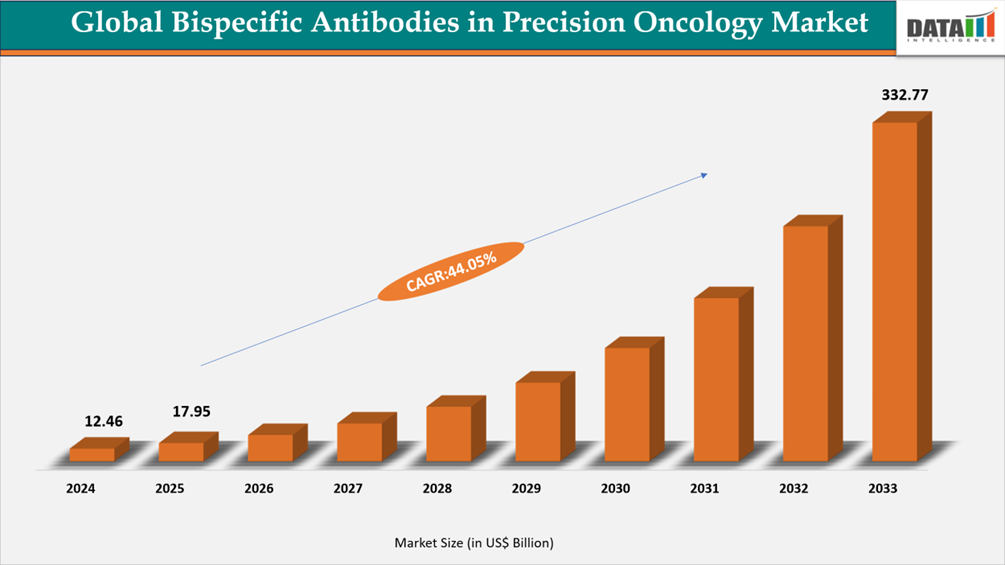

The global bispecific antibodies in precision oncology market reached US$12.46 Billion in 2024, rising to US$17.95 Billion in 2025 and is expected to reach US$332.77 Billion by 2033, growing at a CAGR of 44.05% from 2026 to 2033.

The rising incidence of cancer worldwide, the quick development of immuno-oncology, and the growing clinical efficacy of targeted biologic treatments are the main factors driving market expansion. The growing incidence of solid and hematologic malignancies globally is driving the market. Global cancer incidence reached almost 20 million new cases in 2022, according to World Health Organization cancer data, and is predicted to continue to rise as a result of aging populations and risk factors associated with lifestyle. Bispecific antibodies are becoming more popular because they may target immune effector cells and tumor-associated antigens at the same time, increasing treatment specificity and therapeutic results.

Increasing regulatory approvals, the growth of precision medicine, and rising investment in cancer biologics research by top pharmaceutical companies contribute to hastening market acceptance. Continued pipeline expansion, combination therapy methods, and the development of next-generation multi-specific antibodies are likely to drive long-term growth in precision oncology applications worldwide.

Bispecific Antibodies in Precision Oncology Industry Trends and Strategic Insights

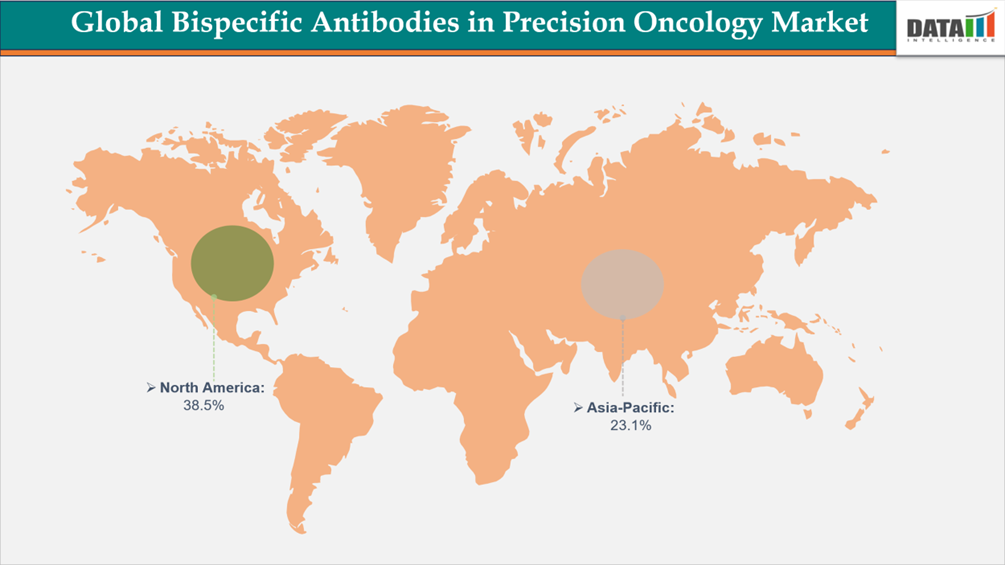

- North America leads the global bispecific antibodies in precision oncology market, capturing the largest revenue share of 38.5% in 2025.

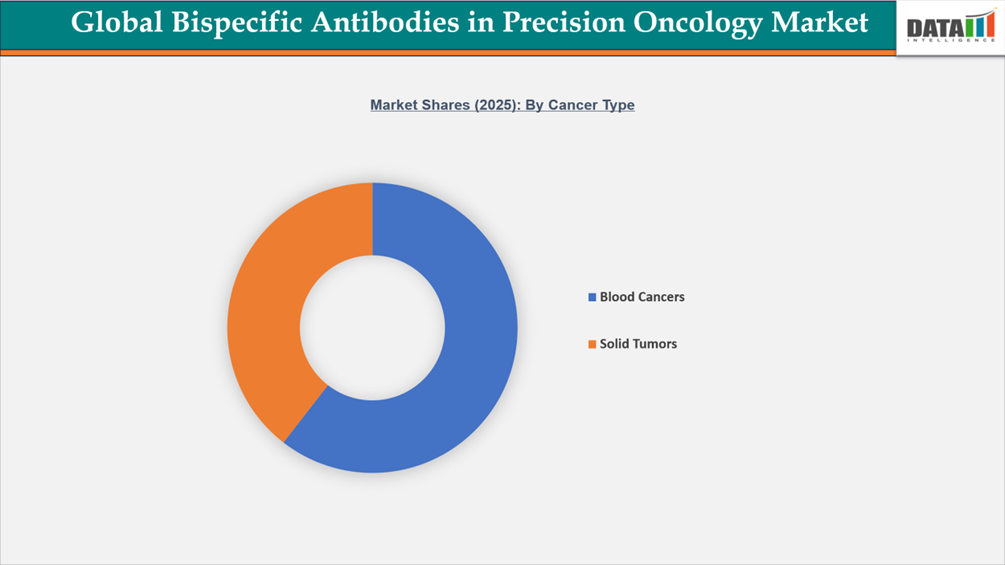

- By cancer type, blood cancers led the global bispecific antibodies in precision oncology market, capturing the largest revenue share of 60.5% in 2025.

Global Bispecific Antibodies in Precision Oncology Market Size and Future Outlook

- 2025 Market Size: US$17.95 Billion

- 2033 Projected Market Size: US$332.77 Billion

- CAGR (2026–2033): 44.05%

- Dominating Market: North America

- Fastest Growing Market: Asia-Pacific

For More Detailed Information, Download Sample

Market Dynamics

Rising Demand for Precision and Targeted Oncology Therapies

The growing emphasis on precision oncology is a primary driver for the worldwide bispecific antibody market. According to the WHO, cancer caused almost 20 million new cases worldwide in 2022, with the incidence anticipated to increase to around 35 million cases per year by 2050, considerably boosting the demand for more effective and tailored treatment options.

According to the U.S. FDA, biomarker-driven medicines have accounted for around 43% of newly approved cancer drugs in recent years, indicating the growing emphasis on personalized therapy strategies. Advances in molecular diagnostics and biomarker profiling have allowed healthcare professionals to discover tumor-specific antigens and genetic changes, raising the demand for highly targeted medicines that increase efficacy while reducing systemic toxicity. Bispecific antibodies, which bind tumor-associated antigens and immune effector cells (such as CD3 on T-cells), are well aligned with this therapeutic paradigm because they provide more selectivity and immunological activation than standard monoclonal antibodies do.

Segmentation Analysis

The global bispecific antibodies in precision oncology market is segmented based on cancer type, mechanism of action, target/biomarker, line of therapy, route of administration, end user, and region.

Dominance of Blood Cancers Driven by Strong Clinical Validation and Early Regulatory Approvals

The market for bispecific antibodies in precision oncology is primarily driven by blood cancers due to their well-defined target biology, early regulatory approvals, and robust clinical validation. Several first-in-class bispecific antibodies, including Blincyto, Tecvayli, and Elrexfio, have received approvals from the U.S. FDA and the European Medicines Agency for hematologic malignancies such as acute lymphoblastic leukemia and multiple myeloma. Hematologic indications account for approximately 60.5% of the total worldwide bispecific antibody revenue, indicating earlier commercialization and broader clinical utilization.

According to WHO and GLOBOCAN cancer statistics, leukemia, lymphoma, and multiple myeloma account for roughly 1.3 million new cases globally in 2022, highlighting the large patient pool driving treatment demand. Furthermore, statistics from the US National Institutes of Health clinical trial registry show that a significant fraction of late-stage bispecific antibody studies have traditionally focused on blood malignancies, supporting development concentration in this market. Accelerated approval pathways, orphan drug incentives, and strong inclusion in treatment guidelines have collectively positioned blood cancers as the leading revenue-generating segment in the global bispecific antibody precision oncology market, while solid tumors represent a rapidly expanding area of research, aided by advanced biomarker-driven targeting strategies and next-generation bispecific platforms.

Geographical Penetration

Largest Market:

Demand for Bispecific Antibodies in Precision Oncology Market in North America

North America dominates the global bispecific antibodies in precision oncology market because of its high cancer burden, sophisticated healthcare infrastructure, strong regulatory approval, and early acceptance of new biologics. The region accounts for 38.5% of the global market share, reflecting its leadership in oncology drug commercialization and clinical innovation. North America leads the worldwide bispecific antibodies precision oncology market in terms of revenue generation due to high oncology medication spending, extensive biomarker testing usage, robust reimbursement systems, and quick incorporation into treatment recommendations. Additionally, the strong presence of leading biopharmaceutical companies and active clinical development pipelines further reinforces the region’s dominant market position.

U.S. Bispecific Antibodies in Precision Oncology Market Outlook

In the United States, the future for bispecific antibodies in precision oncology remains extremely promising, driven by a considerable burden of hematologic and solid cancers and robust uptake of biomarker-guided immunotherapies. According to the American Cancer Society, the United States is expected to report around 2,001,140 new cancer cases in 2024, resulting in a large suitable patient pool for targeted immunotherapies. The United States Food and Drug Administration has issued various approvals, breakthrough treatment designations, and accelerated avenues for bispecific antibodies, allowing for faster commercialization.

Furthermore, the United States dominates worldwide cancer clinical research activity, with a large number of bispecific antibody studies listed in the National Institutes of Health clinical trial database. High biomarker testing rates, substantial oncology clinical trial activity, solid reimbursement systems, and increasing combination use with checkpoint inhibitors significantly contribute to the United States' position as a significant revenue driver in the worldwide bispecific antibodies precision oncology market.

Canada Bispecific Antibodies in Precision Oncology Market Trends

In Canada, the need for bispecific antibodies in precision oncology is increasing in tandem with the country's growing cancer burden and increased usage of biomarker-based medicines. The Canadian Cancer Statistics 2023 study indicates that around 2 in 5 Canadians will get cancer throughout their lifetime. Hematologic malignancies, lung cancer, breast cancer, and colorectal cancer are major therapeutic areas for targeted immunotherapies. The growing use of precision diagnostics, including HER2, EGFR, and hematologic indicators like CD19 and BCMA, is increasing eligibility for bispecific antibody therapies. The increased integration of precision diagnostics, as well as expanded public reimbursement approvals through Health Canada, ultimately contribute to long-term market development.

Fastest Growing Market:

Asia-Pacific Records the Fastest Growth in the Bispecific Antibodies in Precision Oncology Market

Asia-Pacific is developing as the fastest-growing region in the bispecific antibodies in the precision oncology market, owing to a rapidly rising cancer burden and increased access to innovative biologic medicines. According to GLOBOCAN (2022) estimates released by the International Agency for Research on Cancer, Asia accounts for about half of worldwide cancer incidence, with significant increases in lung, breast, colorectal, gastric, and hematologic malignancies in China, India, Japan, and South Korea. Rising aging populations, urbanization, and lifestyle changes are all leading to steady rises in oncology cases throughout the area.

Simultaneously, hospital infrastructure investment, expanded biomarker testing capabilities, and regulatory acceleration for novel biologics are enhancing access to precision immunotherapy. Growing involvement in worldwide clinical trials, as well as increased local biopharmaceutical production capacity, helps to drive regional market growth.

India Bispecific Antibodies in Precision Oncology Market Insights

India's growing cancer rate and steady development of sophisticated oncology care infrastructure are driving the country's bispecific antibody market in precision oncology. According to the Indian Council of Medical Research and the National Cancer Registry Program, in 2022, over 1.5 million new cancer cases were reported in India, with breast, lung, colorectal, and hematologic malignancies being key targets for precision immunotherapies such as bispecific antibodies.

Access to high-cost biologics remains concentrated in urban centers, but expanding oncology infrastructure, wider biomarker testing, and improved screening programs are steadily increasing eligibility and access to bispecific antibody therapies in India.

China Bispecific Antibodies in Precision Oncology Market Industry Growth

The market for bispecific antibodies in precision oncology is growing quickly in China due to the country's high and rising cancer incidence. The International Agency for Research on Cancer's GLOBOCAN 2022 estimates that China had a significant number of new cancer cases worldwide, at about 4.82 million. The main indications and important targets for the development of bispecific antibodies were lung, breast, colorectal, gastric, liver, and hematologic malignancies.

Rising cancer rates, increased use of biomarker testing, and rapid regulatory changes under the National Medical Products Administration are allowing for quicker implementation of new biologics. Expanded public insurance coverage, as well as the inclusion of innovative cancer medications on the National Reimbursement Drug List, are helping to improve treatment accessibility. Collectively, these demographic, regulatory, and healthcare advancements position China as a major growth engine in the global bispecific antibodies precision oncology market.

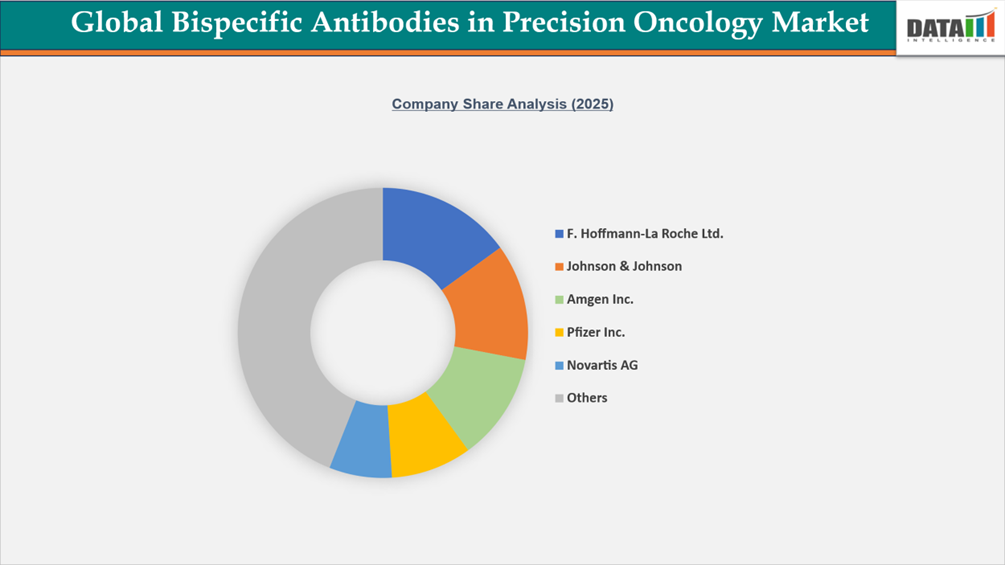

Competitive Landscape

The global market for bispecific antibodies in precision oncology is extremely competitive and innovation-driven, with major biopharmaceutical firms such as F. Hoffmann-La Roche Ltd.*, Johnson & Johnson, Amgen Inc., Pfizer Inc., and Novartis AG leading in the field. These companies retain their dominance through sophisticated bispecific antibody technologies, substantial cancer pipelines, and significant worldwide commercialization capabilities.

Other key players, including Bristol-Myers Squibb Company, Merck & Co., Inc., Eli Lilly and Company, AbbVie Inc., and AstraZeneca, are expanding their market presence through strategic collaborations, targeted acquisitions, and the development of next-generation bispecific and multispecific antibody programs.

Competition is fostered by fast innovation in T-cell engager technologies, dual checkpoint and tumor-targeting techniques, and growth into solid tumor indications. Companies are competing for the bispecific antibodies precision oncology market by investing heavily in R&D, developing sophisticated biologics manufacturing capabilities, forming strategic alliances, and establishing worldwide commercialization networks.

Key Developments

- In February 2025, AbbVie Inc. entered into a collaboration with Xilio Therapeutics to develop masked T-cell engagers designed for tumor-selective activation, involving $52 million upfront and up to USD 2.1 billion in potential milestone payments.

- In March 2025, Sanofi agreed to acquire rights to Dren Bio’s bispecific antibody, a myeloid cell engager aimed at deep B-cell depletion, with $600 million upfront and up to USD 1.9 billion in total deal value, strengthening its immunology and oncology pipeline.

- In January 2025, InnoCare Pharma and KeyMed Biosciences announced a licensing agreement with Prolium for the CD20×CD3 bispecific antibody ICP-B02, expanding global development and commercialization opportunities.

What Sets This Global Bispecific Antibodies in Precision Oncology Market Intelligence Report Apart

- Latest Data & Forecasts – Comprehensive and up-to-date market intelligence with forecasts through 2033, covering global demand in terms of market value by cancer type, mechanism of action, target/biomarker, line of therapy, route of administration, end user, and region, including detailed analysis across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa.

- Regulatory Intelligence – In-depth assessment of global biologics regulatory frameworks impacting bispecific antibody development and commercialization, including requirements from FDA, EMA, NMPA, PMDA, and CDSCO, accelerated approval pathways, breakthrough therapy designations, biologics license applications (BLA), and post-marketing pharmacovigilance obligations.

- Competitive Benchmarking – Structured benchmarking of leading biopharmaceutical companies based on bispecific platform technologies, clinical pipeline strength, approved product portfolio, geographic reach, pricing strategies, manufacturing capabilities, and strategic collaborations in precision oncology.

- Geographic & Emerging Market Coverage – Regional analysis highlighting cancer incidence trends, immuno-oncology adoption rates, reimbursement landscapes, biologics accessibility, and growth opportunities in emerging markets across Asia-Pacific, Latin America, and the Middle East.

- Actionable Strategies & Cost Dynamics – Strategic insights into lifecycle management, combination therapy positioning, solid tumor expansion strategies, biologics manufacturing cost structures, cold-chain logistics considerations, and pricing pressures, supported by expert perspectives from oncology specialists, regulatory advisors, and biopharma executives.