Biosimilars Market Size & Growth

Biologic drug spending is placing sustained pressure on healthcare budgets, creating a stronger commercial case for biosimilars across oncology, immunology, endocrinology and other specialty therapy areas. Biosimilars are becoming a strategic priority for payers, public health systems, hospital procurement teams and pharmaceutical companies because they can improve access to biologic therapies while lowering treatment costs compared with originator biologics.

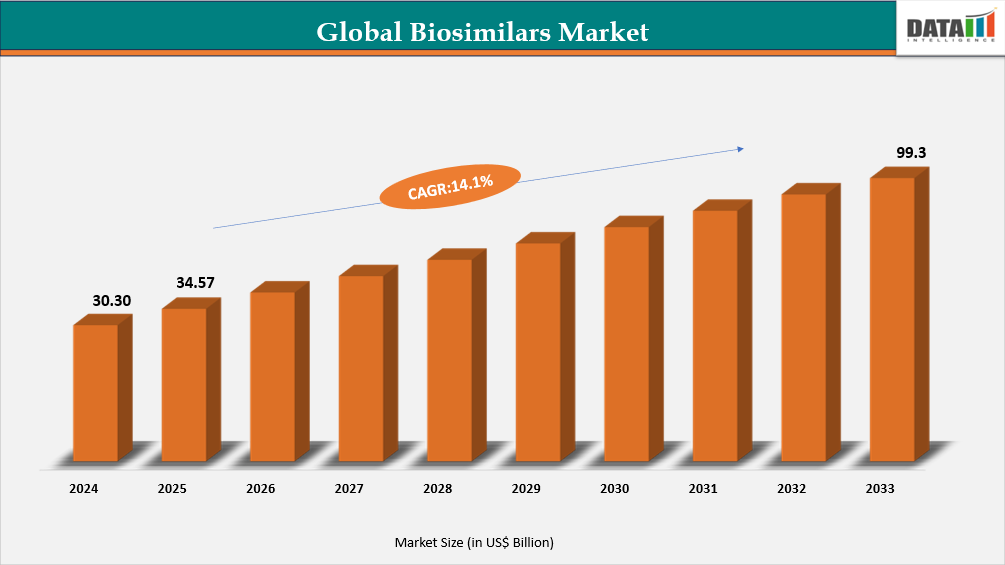

Biosimilars Market is valued at US$ 34.57 billion in 2025 and is projected to reach US$ 129.29 billion by 2035, growing at a CAGR of 14.1% during 2026–2035.

The market matters now because multiple blockbuster biologics in oncology, immunology and diabetes have lost or are approaching patent expiry, opening high-value opportunities for biosimilar developers. More than 45 biosimilars had been approved in the U.S. by 2025, and more than 300 biosimilar candidates are reported to be in clinical development globally. For business decision-makers, the investment timing is significant because payer-led substitution, government tendering, reimbursement reforms and regional manufacturing expansion are all improving the commercial pathway for biosimilar adoption.

Biosimilars Market Scope

| Report Attribute | Details |

| Market Size in 2025 | US$34.57 billion |

| Market Size by 2035 | US$129.29 billion |

| CAGR | 14.1% |

| Historic Years | 2023 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

| Segments Covered | Drug Class, Therapeutic Area, Manufacturing Modality, Route of Administration, End User and Region |

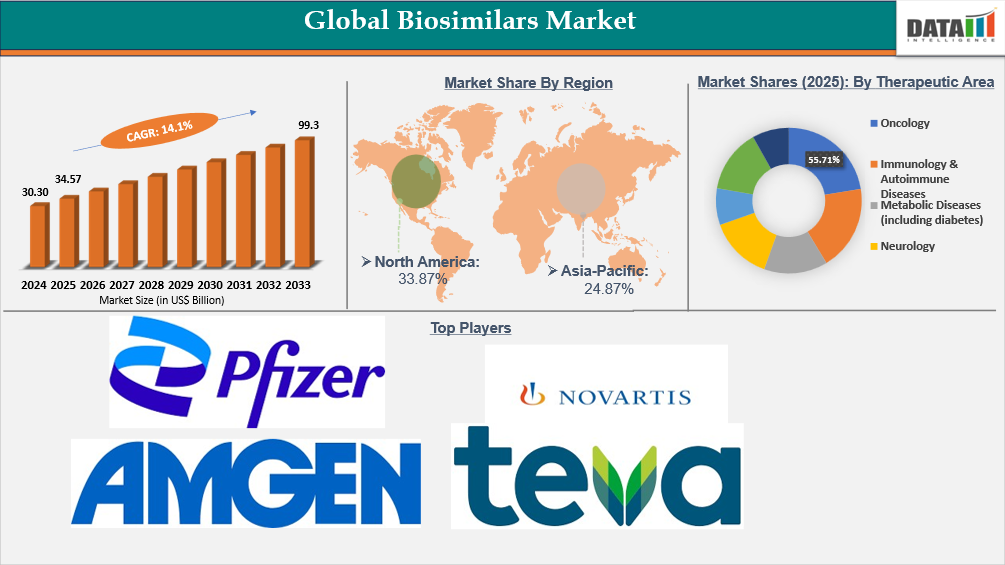

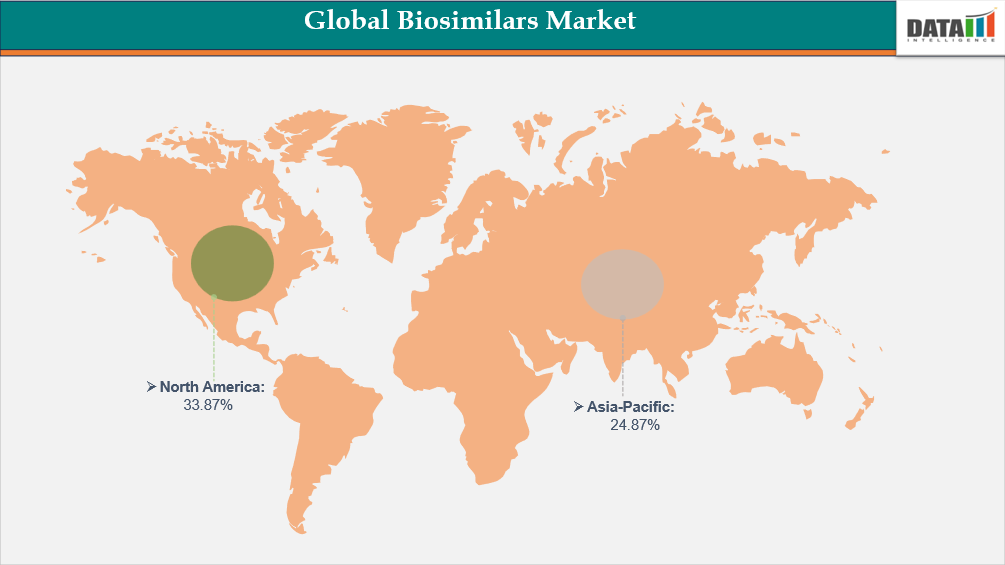

| Leading Region | North America, with 33.87% revenue share in 2025 |

| Fastest Growing Region | Asia-Pacific |

Biosimilars Market Key Takeaways

- The Biosimilars Market 2026 value is recalculated at US$39.44 billion, signaling strong near-term expansion as payers intensify pressure on biologic drug costs.

- The Biosimilars Market 2035 forecast reaches US$129.29 billion, supported by a 14.1% CAGR and continued entry of biosimilars for high-value biologic targets.

- North America held the largest Biosimilars Market Share at 33.87% in 2025, supported by FDA approvals, payer incentives and growing adoption across oncology and autoimmune disease care.

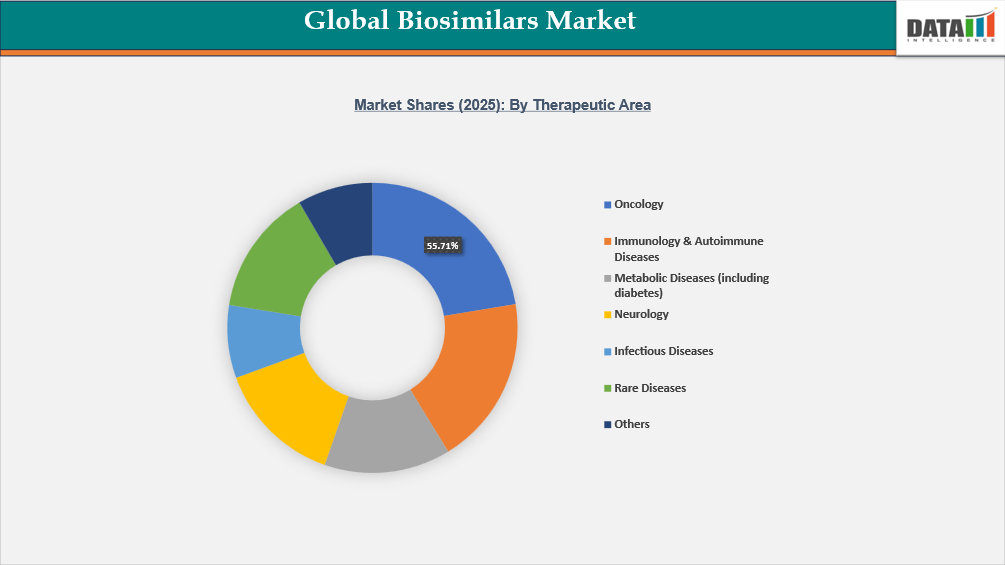

- Oncology led by therapeutic area with 55.71% revenue share in 2025, reflecting heavy use of monoclonal antibodies and the patent expiry of major cancer biologics.

- Asia-Pacific is the fastest-growing region, supported by large patient populations, domestic manufacturing scale, regulatory reforms and lower-cost biologic access strategies.

- Government tendering and biosimilar switching programs are becoming powerful adoption tools, especially where public health systems use centralized procurement.

- Competition is intensifying as Pfizer, Amgen, Sandoz, Samsung Bioepis, Celltrion, Biocon, Viatris, Dr. Reddy’s Laboratories and other companies target oncology, immunology and metabolic disease portfolios.

Biosimilars Market Dynamics: Payer Pressure, Patent Loss and Procurement Reform

Public Health Systems Are Using Biosimilars to Control Specialty Drug Spending

Government-led switching and tender policies are among the strongest drivers of Biosimilars Market Growth. Public health systems in several countries are using centralized tendering to purchase biologics at scale, often awarding contracts to lower-priced biosimilars and encouraging hospitals to transition from originator biologics. In some European health systems, biosimilar market share has exceeded 70% to 80% for selected molecules within a few years of tender implementation.

These procurement models are commercially important because they convert biosimilar adoption from a physician-by-physician decision into a system-level purchasing strategy. For governments and payers, the savings can be redirected toward broader treatment access. For manufacturers, winning tenders can rapidly expand volume, although it may also intensify price competition.

Patent Expiries Are Expanding the Addressable Market

Biosimilar developers are benefiting from the loss of exclusivity of major biologics used in oncology, immunology and diabetes. Originator biologics represent a large share of pharmaceutical expenditure in developed markets, and the arrival of biosimilars creates a route for hospitals and payers to reduce cost without removing access to advanced biologic therapies.

The pipeline outlook is also strong. More than 300 biosimilar candidates are reported to be in different stages of clinical development worldwide. This pipeline depth indicates that the market is not dependent on a small number of molecules. Instead, growth through 2035 is expected to be supported by multiple therapeutic areas, broader regulatory acceptance and regional commercialization partnerships.

Physician Confidence and Reimbursement Design Are Improving Adoption

Clinical acceptance is improving as physicians, hospitals and payers gain more experience with biosimilar safety, efficacy and switching outcomes. Increasing inclusion of biosimilars in clinical treatment guidelines and reimbursement frameworks is making adoption more routine in hospital and specialty care settings.

However, uptake can still vary by country, molecule and care setting. Barriers include physician caution, patient concerns around switching, pricing pressure, supply reliability and payer-specific formulary rules. Companies that invest in medical education, real-world evidence, supply continuity and payer engagement are better positioned to convert approvals into commercial adoption.

Biosimilars Market Market Opportunities

The most attractive opportunities are concentrated around high-cost biologics with large patient populations and meaningful payer pressure. Oncology remains the highest-value opportunity because monoclonal antibody therapies are widely used, expensive and increasingly exposed to biosimilar competition. Biosimilars for trastuzumab, bevacizumab, rituximab and future pembrolizumab candidates are strategically important because they target large oncology expenditure pools.

Manufacturers have a strong opportunity in cost-efficient biologics production. Companies with scalable monoclonal antibody manufacturing, quality systems, regulatory capability and global commercialization partners can compete more effectively in tender-driven and payer-managed markets. Regional partnerships are also becoming important, especially in the Middle East, North Africa and Asia-Pacific, where local access and commercialization infrastructure influence adoption.

Investors should track companies with late-stage oncology biosimilar pipelines, proven manufacturing capacity, strong regulatory execution and commercial agreements in both developed and emerging markets. Procurement teams should monitor biosimilar availability by molecule, supply reliability, switching policy, reimbursement status and expected price competition.

Economic and Investment Analysis

Macroeconomic pressure on healthcare spending is a major factor supporting the biosimilars market. Biologics account for a high share of specialty drug expenditure, and in the U.S., biologics account for more than 40% of total Medicare Part B drug spending despite representing a small share of prescriptions. This creates a clear financial incentive for biosimilar substitution.

Investment trends are focused on monoclonal antibody production capacity, biosimilar development platforms, regulatory submissions, clinical development partnerships and regional commercialization agreements. Capital expenditure is meaningful because biosimilar manufacturing requires specialized biologics infrastructure, quality controls and regulatory compliance. However, the payoff can be attractive where products target blockbuster biologics with large annual sales.

ROI depends on launch timing, tender access, pricing strategy, manufacturing efficiency, payer coverage and physician adoption. Economic risks include aggressive price erosion, delayed approvals, manufacturing complexity, litigation, switching resistance and procurement concentration in public markets.

Biosimilars Market Segmentation Analysis

The Biosimilars Market Report is segmented by Drug Class, by Therapeutic Area, by Manufacturing Modality, by Route of Administration, by End User, and by Region - Share, Trends, and Forecast to 2035.

Oncology Remains the Commercial Anchor

Oncology accounted for 55.71% of the Biosimilars Market Share in 2025. Based on the 2025 market value, this represents approximately US$19.26 billion. The segment leads because biologic therapies, especially monoclonal antibodies, are widely used in cancer care and represent a major share of oncology treatment cost.

Globally, more than 20 million new cancer cases are diagnosed each year, creating sustained demand for effective and affordable biologic therapies. In the U.S. alone, more than 1.9 million new cancer cases are diagnosed annually. Biosimilar competition has reduced prices for certain oncology biologics by 30% to 60% in European public health settings, improving the ability of healthcare systems to treat more patients within fixed budgets.

Immunology, Diabetes and Other Specialty Areas Add Pipeline Depth

Immunology remains a major opportunity because biologics used for autoimmune diseases are high-cost, chronic therapies. Biosimilar adoption in this area depends heavily on payer policy, physician confidence and switching frameworks. Diabetes and endocrinology also represent important demand areas, particularly where insulin biosimilars and other biologic alternatives can support access and affordability.

End users include hospitals, cancer centers, specialty clinics, public health systems and pharmacy benefit organizations. Hospitals and public procurement bodies are especially influential because many biosimilars are used in institutional settings where formularies and tenders drive purchasing behavior.

Manufacturing Modality and Route of Administration Influence Competitive Strategy

Manufacturing modality is strategically important because biosimilars require highly controlled biologics production, analytical comparability and regulatory validation. Companies with efficient manufacturing platforms can compete more effectively in price-sensitive tenders.

Route of administration also matters commercially. Injectable and infusion-based biosimilars often flow through hospital and specialty care channels, where procurement decisions are centralized. This makes hospital access, supply assurance and payer contracts essential to market penetration.

Biosimilars Market Geographical Penetration

North America Leads the Global Biosimilars Market

North America led the global market with 33.87% revenue share in 2025. Based on the 2025 global market size, the region represented approximately US$11.71 billion. Adoption is accelerating due to payer efforts to reduce biologic drug spending, FDA approvals and wider physician experience with biosimilars.

In the U.S., more than 45 biosimilars had been approved by 2025 across oncology, immunology and endocrinology. Biosimilars referencing filgrastim and trastuzumab have gained meaningful uptake in hospital oncology settings, supported by payer incentives and clinical equivalence evidence. The Inflation Reduction Act has also increased scrutiny of high-cost biologics, indirectly strengthening interest in lower-cost biosimilar alternatives.

Canada’s market is driven by provincial switching policies and reimbursement reforms. British Columbia and Alberta have reported switching rates exceeding 80% for selected biologics after mandatory transition initiatives. Ontario and Quebec have also implemented biosimilar transition programs covering products such as insulin glargine, infliximab and etanercept. These policies are supporting utilization across public plans and hospital procurement systems.

Europe Remains the Most Mature Tender-Based Adoption Market

Europe has one of the most established biosimilar regulatory and procurement ecosystems. The region has historically led early adoption through centralized approvals, public tenders and strong payer involvement. Tender systems and therapeutic substitution policies have enabled high uptake in selected biologic categories, particularly oncology and anti-TNF therapies.

For companies, Europe offers volume potential but also exposes manufacturers to intense price competition. Winning tenders can rapidly increase adoption, but pricing discipline, supply reliability and portfolio breadth are critical. European hospital systems are expected to continue using biosimilars as a tool to manage specialty drug budgets and increase treatment access.

Asia-Pacific Is the Fastest-Growing Region in Biosimilars Market

Asia-Pacific is the fastest-growing biosimilars market, supported by large patient populations, manufacturing expansion and policy efforts to improve access to lower-cost biologics. The region accounts for more than 60% of the global population, creating large demand for affordable biologic therapies across oncology, autoimmune disease and metabolic disorders.

China and India are major growth markets. China reports more than 4.8 million new cancer cases annually and has approved over 30 biosimilars in recent years. Centralized procurement and national reimbursement price negotiations are encouraging hospitals to use cost-effective alternatives. India has approved more than 100 biosimilar products across therapeutic categories and exports biosimilars to more than 100 countries. The country’s biologics manufacturing base, expanding tertiary care infrastructure and growing insurance coverage support long-term demand.

Japan and South Korea are also important due to regulatory maturity, domestic biologics expertise and regional manufacturing capacity. South Korea is particularly relevant because companies such as Samsung Bioepis and Celltrion are active global biosimilar competitors.

Country-Level Market Analysis

The U.S. remains the largest country-level opportunity within North America due to FDA approval momentum, large biologic spending and strong payer influence. The key growth drivers include oncology biosimilar uptake, formulary inclusion, group purchasing organization adoption and policy pressure on high-cost biologics. Barriers include litigation risk, interchangeability considerations, payer complexity and variable physician adoption.

Canada’s market is shaped by provincial reimbursement policy. Mandatory or strongly encouraged switching programs have materially increased biosimilar use in selected provinces. Future opportunities are linked to broader public plan alignment, hospital procurement and national cost-containment discussions.

China offers scale and policy momentum. Large cancer incidence, expanding domestic biopharmaceutical manufacturing and centralized reimbursement negotiations support demand. The main challenges include price pressure, regulatory competition and the need for sustained quality assurance.

India is both a production and consumption hub. With more than 100 approved biosimilar products and exports to over 100 countries, Indian companies are positioned for cost-competitive supply. Domestic uptake is supported by rising cancer burden, hospital expansion and improving insurance coverage, while challenges include affordability constraints and uneven access across public and private healthcare systems.

Regulatory and Policy Analysis

Regulatory confidence is a critical enabler of biosimilar adoption. The U.S. FDA, EMA, Health Canada, China’s National Medical Products Administration and regulators across Asia-Pacific have expanded biosimilar approval pathways and guidance frameworks. The U.S. FDA approved a record 19 biosimilars in 2024, reflecting stronger regulatory throughput and greater confidence in biosimilar review processes.

Government initiatives and reimbursement policies are equally important. Tender-based procurement, biosimilar-first formularies, switching policies, public plan transition programs and national price negotiations are shaping market access. In publicly funded systems, biosimilars are increasingly treated as a budget management tool, not only as a product substitution option.

Expected policy changes are likely to focus on interchangeability, evidence standards, pharmacovigilance, pricing transparency and broader access to biologics. Companies will need strong regulatory documentation, manufacturing consistency and post-market safety monitoring to compete effectively.

Regional Innovation Momentum Index

| Region | Innovation Strength | Pipeline / Innovation Activity | Adoption & Healthcare Impact Indicators |

| North America (U.S.) | FDA approved a record 19 biosimilars in 2024, reflecting accelerating regulatory throughput and policy reforms to simplify interchangeability pathways. | Over 38 biosimilar applications under review globally, with strong participation from companies targeting U.S. approvals. | Biosimilars have generated tens of billions of dollars in healthcare savings in the U.S., supporting payer-driven adoption and formulary expansion. |

| Europe | EMA historically approved 55+ biosimilars over the early development phase of the market, establishing Europe as the most mature regulatory ecosystem. | Strong tender-based procurement systems and early patent expiries continue to stimulate biosimilar launches across oncology and immunology. | Several European health systems report high therapeutic substitution rates, especially in oncology and anti-TNF therapies, reinforcing sustained uptake. |

Asia-Pacific (China,India, South Korea) | National regulators have issued biosimilar development guidelines and accelerated review pathways to support domestic manufacturing expansion. | Rapid increase in local manufacturers and biologics production capacity, particularly in China and India, with companies exporting to regulated markets. | Lower-cost biosimilars are increasingly used to expand access to biologic therapies in oncology and autoimmune diseases across public healthcare systems. |

Biosimilars Market Competitive Landscape

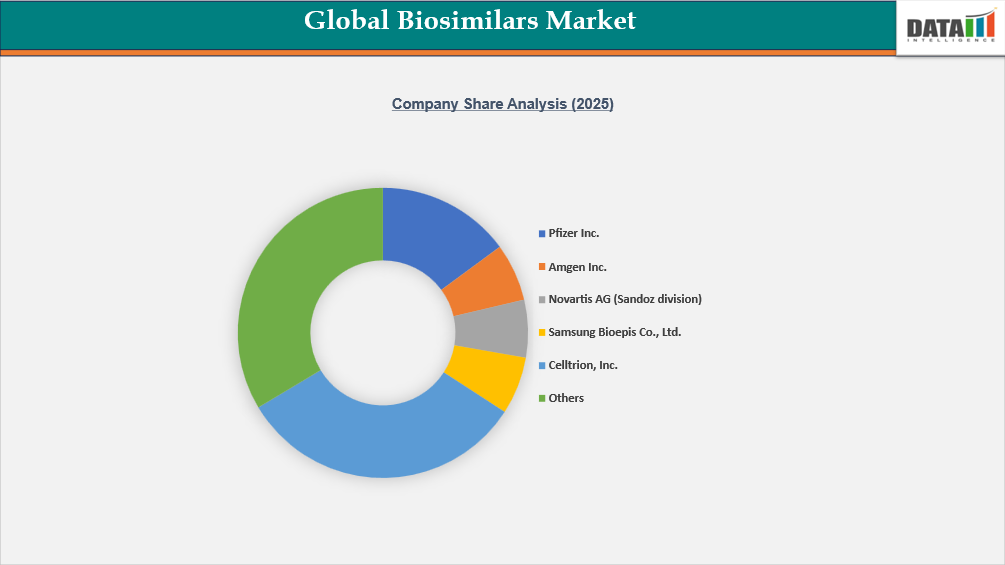

The global biosimilars market is highly competitive, with multinational pharmaceutical companies and specialized biosimilar developers competing across oncology, immunology and metabolic disease areas. Key companies include Pfizer Inc., Amgen Inc., Novartis AG through Sandoz, Samsung Bioepis Co., Ltd., Celltrion, Inc., Biocon Limited, Viatris Inc., Teva Pharmaceutical Industries Ltd., Dr. Reddy’s Laboratories Ltd., STADA Arzneimittel AG, Fresenius Kabi AG, Boehringer Ingelheim International GmbH, Merck KGaA and F. Hoffmann-La Roche Ltd.

Pfizer, Amgen, Sandoz, Samsung Bioepis and Celltrion have strong positions in monoclonal antibody and oncology biosimilars. Biocon, Viatris and Dr. Reddy’s Laboratories are strengthening competitiveness through cost-efficient manufacturing, emerging-market reach and global commercialization partnerships. STADA and Fresenius Kabi are leveraging hospital relationships and regional distribution networks in Europe.

Competitive differentiation is moving beyond product approval. Companies are competing on manufacturing scale, tender pricing, supply reliability, payer engagement, clinical education, portfolio breadth and regional commercialization access. As more biosimilars enter high-value biologic categories, pricing pressure will increase, making manufacturing efficiency and market access strategy decisive.

Investment Landscape

Samsung Bioepis expanded biosimilar manufacturing capacity in South Korea in 2025 to support oncology and immunology pipelines. This improves global supply capability and strengthens Asia-Pacific export potential.

- Biocon invested in expanding biologics and biosimilar production facilities in Bengaluru in 2025 to scale monoclonal antibody output. The investment supports cost-competitive supply and strengthens participation in global tenders.

| Company | Year | Development | Impact on Market | |

| Samsung Bioepis Co., Ltd. | 2025 | Expanded biosimilar manufacturing capacity in South Korea to support oncology and immunology pipelines. | Increased global supply capability and strengthened Asia-Pacific export potential. | |

| Biocon Ltd | 2025 | Invested in expanding biologics and biosimilar production facilities in Bengaluru to scale monoclonal antibody output. | Improved cost-competitive supply and supported global tender participation. | |

Recent Developments in Biosimilars Market

- June 2026 – Samsung Bioepis expands global biosimilar portfolio

Samsung Bioepis strengthened its biosimilar business by advancing regulatory approvals and commercialization activities for immunology and oncology biosimilars, while expanding strategic partnerships to increase patient access across global markets. - June 2026 – Celltrion advances next-generation biosimilar commercialization

Celltrion expanded its global biosimilar portfolio through new regulatory filings, market launches, and commercialization initiatives for autoimmune disease and oncology treatments, reinforcing its position in the global biosimilars market. - May 2026 – Sandoz expands biosimilar pipeline and global launches

Sandoz (Novartis spin-off) strengthened its biosimilar portfolio by advancing regulatory submissions and commercial launches for high-value biologics, expanding access to affordable treatments across Europe, North America, and Asia. - May 2026 – Amgen advances oncology and inflammatory disease biosimilars

Amgen expanded its biosimilar portfolio by supporting new global launches and regulatory activities for oncology and inflammatory disease biosimilars, strengthening its long-term biologics strategy. - April 2026 – Biocon Biologics expands international biosimilar footprint

Biocon Biologics strengthened its global commercialization strategy through expanded regulatory approvals, strategic partnerships, and increased manufacturing capacity for insulin, oncology, and immunology biosimilars. - March 2026 – Fresenius Kabi expands biosimilar commercialization strategy

Fresenius Kabi advanced its biosimilars business by expanding product availability, strengthening commercialization partnerships, and increasing access to biosimilar therapies in oncology and autoimmune diseases. - February 2026 – Viatris strengthens global biosimilar business

Viatris expanded its biosimilar portfolio through new commercialization agreements and regulatory milestones, supporting broader patient access to biologic therapies across multiple therapeutic areas.

Strategic Insights and Analyst Perspective

The biosimilars market is entering a more competitive phase where approval alone will not guarantee commercial success. Manufacturers need integrated strategies covering molecule selection, regulatory execution, scalable production, payer engagement, tender participation and physician confidence-building.

For investors, oncology biosimilars and high-value immunology targets remain key areas to monitor. Partnerships targeting pembrolizumab biosimilars indicate that companies are moving toward the next wave of blockbuster biologic opportunities. For payers and procurement teams, biosimilars offer a route to contain biologics spending, but supply security and clinical confidence must remain central to switching programs.

Risk management should focus on pricing erosion, litigation delays, manufacturing quality, policy changes and adoption variability by country. Companies with strong manufacturing economics, broad portfolios and regional commercialization partnerships are likely to outperform single-product competitors.

Report Benefits

This Biosimilars Market Report helps pharmaceutical manufacturers understand patent expiry opportunities, therapeutic area demand and regional adoption dynamics. Investors can assess pipeline attractiveness, market access risk and manufacturing-related value creation. Suppliers and contract manufacturers can evaluate demand for biologics production infrastructure, monoclonal antibody capacity and global supply partnerships. Procurement and payer teams can benchmark biosimilar switching policies, tendering models and cost-saving opportunities. Strategy teams can use the report to assess competitive positioning, product direction and long-term Biosimilars Market Growth through 2035.

What Sets This Global Biosimilars Market Intelligence Report Apart

- Latest Data & Forecasts – Comprehensive and up-to-date market intelligence with forecasts through 2033, covering global demand by key segmentation, with region-wise analysis across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa.

- Regulatory Intelligence – In-depth assessment of global pharmaceutical regulatory frameworks impacting market development and commercialization, including FDA, EMA, NMPA, PMDA, and CDSCO requirements, clinical trial pathways, labeling standards, patent exclusivity, and post-marketing surveillance.

- Competitive Benchmarking – Structured benchmarking of leading innovator and generic manufacturers based on product portfolios, pipeline strength, geographic reach, pricing strategies, clinical differentiation, and partnerships in the market.

- Geographic & Emerging Market Coverage – Regional analysis highlighting key impacting factors, with special focus on growth opportunities in Asia-Pacific, Latin America, and Middle Eastern markets.

- Actionable Strategies & Cost Dynamics – Strategic insights into lifecycle management, generic entry risks, combination therapy positioning, pricing pressures, and manufacturing cost structures, supported by expert perspectives from various specialists, regulatory advisors, and pharmaceutical executives.

Target Audience

- Biosimilar developers

- Pharmaceutical companies

- Biologics manufacturers

- Contract Development and Manufacturing Organizations (CDMOs)

- Hospital procurement teams

- Public health agencies

- Healthcare payers

- Pharmacy Benefit Managers (PBMs)

- Oncology centers

- Specialty clinics

- Investors in biopharmaceutical sector

- Private equity firms

- Venture capital firms

- Regulatory consultants

- Strategy and planning teams

- Product managers

- Market access leaders

Related Reports

The biopharmaceuticals market serves as the foundation for biosimilar development, as biosimilars are developed from reference biologic drugs. Increasing demand for cost-effective biologic therapies, expanding biologics pipelines, and advancements in biomanufacturing are driving growth across both markets. Rising investments in biologic innovation continue to create opportunities for biosimilar manufacturers.

Cell and gene therapies and biosimilars are key components of the evolving biologics landscape. Both markets depend on advanced biotechnology manufacturing, stringent regulatory compliance, and specialized production facilities. Continued innovation in biologic therapeutics is strengthening investments across both sectors.

CDMOs play a vital role in biosimilar development by providing process development, analytical testing, clinical manufacturing, and commercial-scale production services. Increasing outsourcing by pharmaceutical and biotechnology companies is improving manufacturing efficiency while reducing development timelines. Growing biosimilar pipelines are driving demand for specialized biologics manufacturing partners.

Bioprocess technologies are essential for producing high-quality biosimilars through optimized cell culture, purification, and downstream processing. Continuous advancements in bioprocessing improve manufacturing efficiency, product consistency, and regulatory compliance. Rising biologics production is supporting growth across both markets.

Single-use bioprocessing systems are increasingly adopted in biosimilar manufacturing because they improve production flexibility, reduce cleaning requirements, and lower operational costs. These technologies accelerate product development while maintaining stringent quality standards. Growing investments in biologics manufacturing continue to boost market demand.