Automotive Material and Component Testing Market Overview

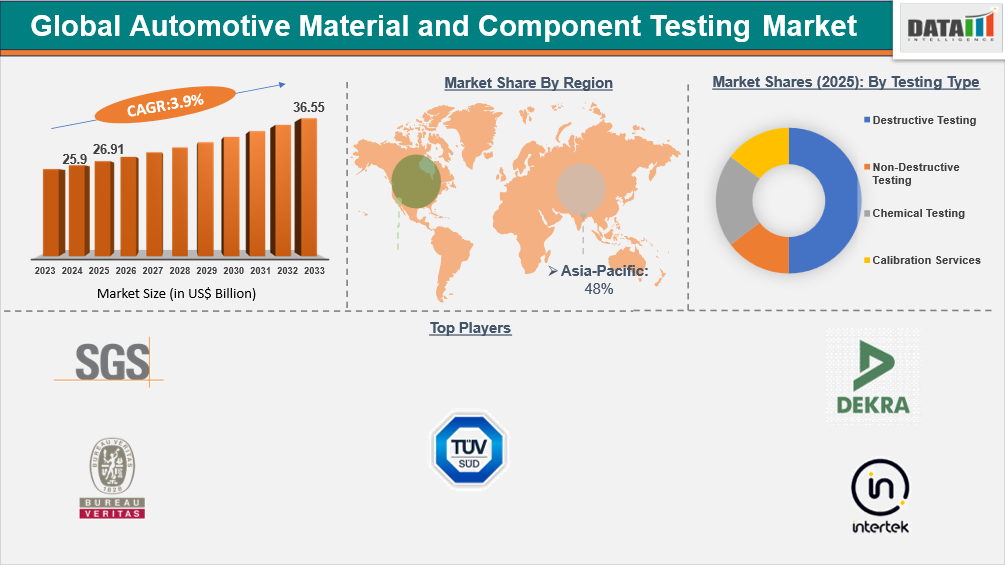

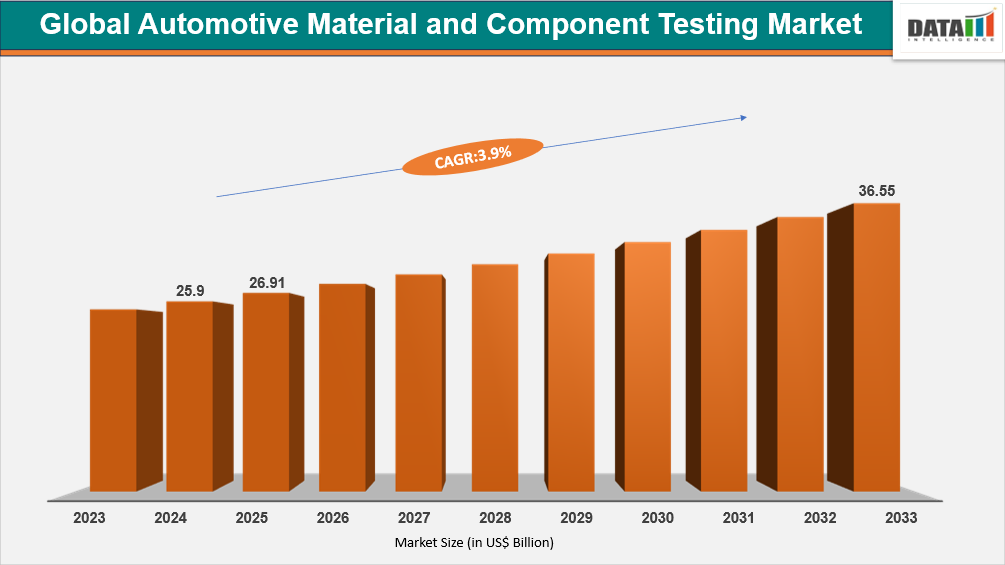

Global Automotive Material and Component Testing Market reached US$ 26.91 billion in 2025 and is expected to reach US$ 36.55 billion by 2033, growing with a CAGR of 3.9% during the forecast period 2026-2033.

The global automotive material and component testing market is a critical segment of the broader automotive testing ecosystem, ensuring vehicle safety, performance, and regulatory compliance. The market is driven by rapid electrification, adoption of lightweight and composite materials, and advanced electronic systems in vehicles. Non-destructive testing (NDT) dominates the market, widely applied for battery modules, structural components, and EV electronics, while chemical testing is the fastest-growing segment, supporting validation of new polymers, battery chemistries, and high-performance alloys. For instance, in March 2025, TÜV SÜD AG, a Germany‑based technical services provider, expanded its test laboratory in Frankfurt am Main, enhancing chemical and product testing capabilities to support broader automotive safety and compliance services.

Automotive material and component testing Industry Trends and Strategic Insights

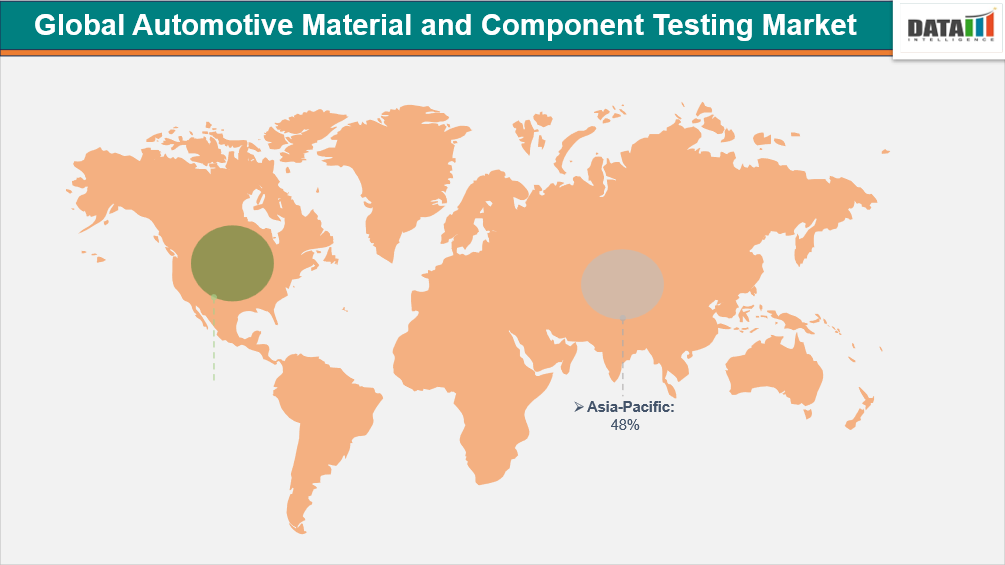

- Asia-Pacific is the dominant and fastest-growing region in the automotive material and component testing market, capturing the share of 48 % in 2025.

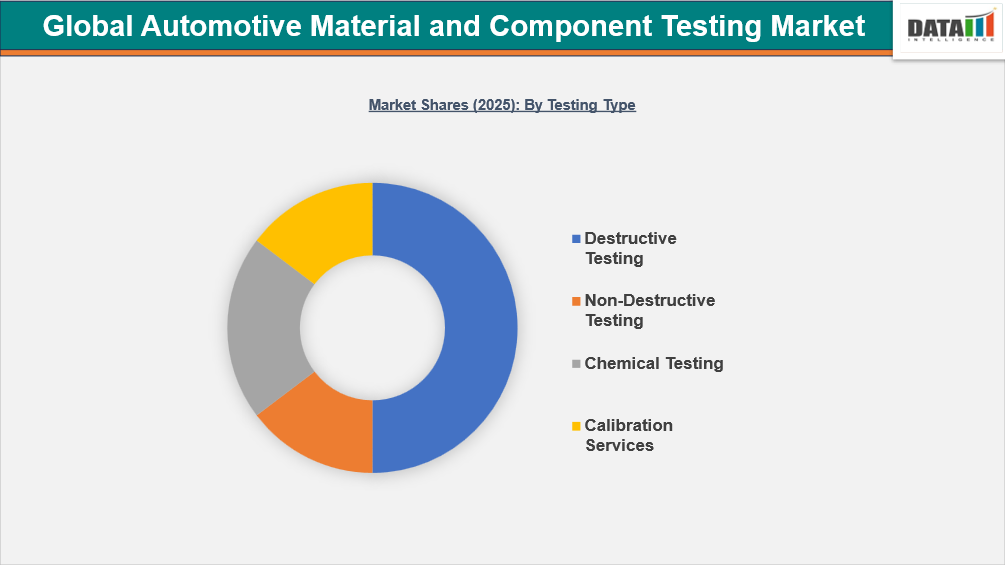

- By testing type, the non-destructive testing is projected to be the largest market, holding a significant share of about 46% in 2025.

Global Automotive material and component testing Market Size and Future Outlook

- 2025 Market Size: US$ 26.91 Billion

- 2033 Projected Market Size: US$ 36.55 Billion

- CAGR (2026-2033): 3.9%

- Largest Market: Asia-Pacific

- Fastest Market: Asia-Pacific

Market Scope

| Metrics | Details |

| By Testing Type | Destructive Testing, Non-Destructive Testing, Chemical Testing, Calibration Services |

| By Application Area | Material, Components |

| By Vehicle Type | Passenger Vehicle, Commercial Vehicle, Off-Highway Vehicle, Two Wheelers, Three Wheelers |

| By Testing Agency | TIC Service Provider, Government Agency, Inhouse Testing or Captive Testing, Others |

| By Project Type | Project Based, Annual Maintenance Contract, One Off Analysis or Walk in Analysis, Others |

| By Region | North America, Latin America, Europe, Asia-Pacific, Middle East and Africa |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth |

Market Dynamics

Rapid EV Adoption and Electrification

The surge in electrified vehicles is reshaping the automotive material and component testing market. Electrified vehicles accounted for 43% of global auto sales by Q1 2025, up from just 9% a few years prior, with China leading at 57% of global BEV registrations, followed by Europe (22%) and the U.S. (12%). This accelerated adoption is driven by government incentives, battery manufacturing scale, and consumer demand for cleaner mobility.

The growing prevalence of EVs is directly increasing the demand for advanced testing services. Components such as batteries, power electronics, inverters, and charging systems require rigorous performance, durability, and safety validation to ensure reliability under varying operating conditions. Forecasts indicate global EV volumes will reach 27.5% of new vehicle sales by 2026, 43.2% by 2030, and over 83% by 2040, while battery demand is projected to exceed 1 TWh in 2025 and hit 6 TWh by 2040. This dramatic increase amplifies the need for specialized material testing, certification, and component validation services, creating a robust growth opportunity for automotive testing providers worldwide.

Long Testing Cycles and High Operational Costs

Automotive material and component testing face significant challenges due to lengthy validation cycles and high operational expenditures. Comprehensive testing of components such as batteries, power electronics, ADAS systems, and structural materials requires sophisticated labs, specialized equipment, and highly trained personnel. These factors contribute to extended testing timelines, often delaying product launches and increasing time-to-market for OEMs and Tier-1 suppliers.

Additionally, the capital-intensive nature of establishing and maintaining testing facilities covering climate chambers, high-voltage battery simulators, vibration rigs, and digital twin platforms drives up operational costs. For smaller testing providers or new entrants, this creates barriers to scale, limiting their ability to compete with established global players like SGS, TÜV SÜD, and Bureau Veritas. Consequently, while EV adoption and component complexity are increasing in demand, the high costs and long cycles act as a market restraint, prompting manufacturers to seek outsourced or collaborative testing solutions to optimize time and investment.

Segmentation Analysis

The global automotive material and component testing market is segmented based on testing type, application area, vehicle type, testing agency, project type, and region.

High-Throughput Non-Destructive Testing and Advanced Imaging Solutions Drive Growth

In 2025, the non‑destructive testing (NDT) segment captured approximately 46% market share, driven by the need to inspect battery modules, structural components, and EV electronics without causing damage. NDT adoption is rising due to increasing EV penetration, lightweight materials, and advanced composite usage across automotive, aerospace, and industrial sectors. High-throughput inspection, real-time fault detection, and digital analytics integration are enabling scalable NDT workflows that improve reliability and reduce product recalls. Commercialization trends include automated inspection lines, AI-assisted defect recognition, and cloud-based data management for large-scale operations.

Technology providers are actively advancing hardware and imaging capabilities to meet this demand. In March 2026, Detection Technology Plc, a Finland‑based industrial imaging solutions company, unveiled the X‑ACE HS high‑speed detector family delivering faster scanning, higher slice coverage, and lower dose for next-generation CT systems that support high-throughput inspection, including NDT applications. This development highlights how companies are enhancing inspection precision and efficiency for automotive components, batteries, and electronics, supporting both mass production scalability and stringent safety compliance requirements.

Advanced Chemical Testing of Battery Chemistries and Lightweight Materials Driving Market Growth

The chemical testing segment is growing rapidly as automotive manufacturers seek precise validation of advanced battery chemistries, polymers, and lightweight composites to ensure performance, safety, and regulatory compliance. Increasing adoption of EVs and hybrid vehicles has intensified the need for chemical characterization of electrodes, electrolytes, coatings, and high-strength alloys. Commercialization trends include lab automation, high-throughput analytical instruments, and integration of spectroscopy and chromatography techniques to enable scalable and reproducible testing workflows. This demand spans industries such as automotive, aerospace, and energy storage, highlighting cross-sector reliance on chemical validation.

Companies are actively advancing chemical testing technologies to meet growing requirements. In February 2025, Anton Paar, an Austria-based laboratory instrumentation company, launched the Litesizer 600 particle size and zeta potential analyzer, enabling faster and more accurate chemical characterization of polymeric and composite materials used in EV batteries and automotive components. This development illustrates how providers are enhancing throughput, precision, and scalability in chemical testing labs, supporting OEMs and Tier-1 suppliers in validating next-generation materials efficiently.

Geographical Penetration

Rapid Electrification and Expanding Testing Infrastructure Propel Asia‑Pacific Leadership

Asia‑Pacific is the largest and fastest-growing region in the global automotive material and component testing market, accounting for approximately 48% of market share in 2025. The region’s dominance is driven by its massive automotive production base, rapid electrification, and increasing adoption of advanced materials and EV technologies. Expanding testing infrastructure, regulatory compliance requirements, and investment in high-throughput NDT and chemical testing labs further reinforce Asia‑Pacific as a global hub for quality assurance and component validation services. OEMs and Tier-1 suppliers in the region are increasingly leveraging automated inspection, digital analytics, and in-line testing systems to optimize production and ensure safety compliance. In November 2025, Volkswagen Group China Technology Company completed its expanded test center in Hefei, China, enabling full local development and validation of batteries, powertrains, and vehicle platforms through comprehensive laboratories and integrated testing workflows.

India Automotive Material and Component Testing Market Outlook

India’s automotive material and component testing market is growing rapidly due to rising EV adoption and increasing complexity of high‑voltage systems in passenger and commercial vehicles. The demand for localized testing infrastructure and specialized training is critical to support OEMs, Tier‑1 suppliers, and service networks. Regulatory emphasis on safety and compliance, combined with investment in testing capabilities, is expanding India’s role in the Asia‑Pacific testing ecosystem. In April 2025, TÜV SÜD South Asia, a Germany‑based testing, inspection, and certification company, launched its e‑Mobility mobile training lab in Bengaluru. The lab provides hands-on high-voltage safety training for engineers and technicians. This initiative enhances India’s testing capabilities and supports scalable EV component validation and compliance.

China Automotive Material and Component Testing Market Trends

China’s automotive material and component testing market is rapidly expanding as EV battery, powertrain, and safety validation become critical to OEM competitiveness and regulatory compliance. Domestic leaders are advancing localized testing and certification to accelerate product introduction and enhance quality assurance across high‑voltage systems and electronics. In April 2025, Contemporary Amperex Technology Co., Limited (CATL), a China‑based battery manufacturer, became the first company to pass China’s new EV traction battery safety standard certification under GB 38031‑2025, reflecting strengthened domestic testing benchmarks and regulatory rigour. This milestone illustrates how global OEMs are investing in China‑specific testing infrastructure to shorten development cycles and support region‑specific product strategies.

Regulatory Analysis

The automotive material and component testing market is guided by strict safety, environmental, and performance regulations worldwide. In the EU, ECE regulations and REACH standards mandate component safety, chemical compliance, and material testing, ensuring high-quality vehicle production. In the US, FMVSS and EPA rules enforce crashworthiness, emissions, and battery safety standards, increasing compliance and testing requirements. In China, GB/T 38031 and related EV battery standards drive rigorous validation of high-voltage systems and materials. India’s AIS and BIS certifications ensure component quality and adherence to domestic and imported vehicle standards. ISO 26262 mandates functional safety testing for electronics and ADAS systems across multiple regions. Accreditation standards like ISO/IEC 17025 ensure testing labs maintain traceable, reliable results. These regulations collectively enhance vehicle safety, environmental compliance, and product reliability while raising operational and testing costs for manufacturers.

Competitive Landscape

- The global automotive material and component testing market is characterized by a competitive landscape that includes both established and regional players.

- Key players include SGS, Bureau Veritas, TÜV SÜD, DEKRA, TÜV Rheinland, Intertek, Underwriters Laboratories, TÜV NORD, Automotive Research Association of India, and Atharva Labs

Key Developments

- In May 2025, Detection Technology Plc, a Finland‑based industrial imaging solutions company, launched the X‑Cargo, pioneering detector modules for high‑speed, high‑energy inspection suitable for advanced NDT of automotive parts and battery systems.

- In April 2025, Detection Technology Plc, a Finland‑based industrial imaging solutions company, introduced the X‑Panel 43108a FQI, a record‑breaking large‑area, high‑speed X‑ray detector for enhanced industrial NDT workflows.

Why Choose DataM?

- Data-Driven Insights: Dive into detailed analyses with granular insights such as pricing, market shares, and value chain evaluations, enriched by interviews with industry leaders and disruptors.

- Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

- White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

- Annual Updates on Purchased Reports: As an existing customer, you enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

- Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. This approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

- Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. This personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. These insights complement and go beyond what is typically available in generic databases.

Target Audience 2026

- Manufacturers/ Buyers

- Industry Investors/Investment Bankers

- Research Professionals

- Emerging Companies